February 2004 – T Theory® Update

Short Range T Update Feb 20 2004

The Short Range T chart shows the developing Cash Build Up Period in the blue volume Oscillator that in a few weeks should lead the S&P and other averages to the normal oversold condition from which a new T’s rally can begin. For this update I have noted three key factors to keep in mind as we move into the next low. Click on the chart for the larger, more detailed image.

The goal of this analysis is to identify the probable starting point for a rally that represents the beginning of a brand new T. This gives the new rally the best upside sustainable trend for the near term, but not necessarily for the very long term, according to T Theory history.

The new T rallies are noted by the red arrows in the upper plot of the S&P 500 adaptive channels. The channel envelopes (the upper red dashed line, the lower green dashed line and the mid black 55 day MA) define overbought and oversold conditions according to a proprietary statistical program I wrote some years ago.

Basically there are two ways to estimate this important low. The first is by referencing the normal channel S&P price levels for a low; secondly by watching the blue volume oscillator for an impending breakout in the Cash Build Up criteria as suggested by a preceding rising bottoms condition. The better procedure is to watch both criteria for clues to the actual turning point. Since none of these conditions is telling me anything significant right now I will await further data.

Nevertheless there are some important observations that can be helpful at this early stage. The latest volume oscillator data suggests the recent rally has peaked out at a lower high implying a loss of upside momentum. This is negative for the near term. However note prior rallies have begun with the volume making a rising bottoms pattern as indicated by the rising red arrowed lines in the lower plot. We can watch for this turning pattern in the weeks ahead after a new oversold condition.

When the pattern of the volume oscillator finally looks ready for a turn, history shows the upper plot of S&P will have weakened enough to bring this benchmark at least down to the 55 day MA level. So a simpler deduction is that the weakening upside momentum will allow the S&P to fall to the 1112 level, the current 55 day MA, or its reading a few weeks later.

Because the MA is rising this eventual downside target may somewhat higher, but at the right time all indicators should become clearer. I still don’t believe the new T’s rally will amount to much more than a trading range.

Terry Laundry

Short Range T Update Feb 12 2004

General Market Summary for Feb 12 2004

This week I am posting my market summary on Friday’s using Thursday’s closing data in anticipation of a long weekend. I will probably use this format going forward as it is more convenient for me as I wind up my week. It also provides a better overall T theory perspective as I am providing the more general 39-week perspective first, and then refine it with the Short Range Ts narrower perspective. The short-term picture may be more precise but has a somewhat greater variability from one week to another. Click on chart below for a larger image.

Turning to the first chart, which presents the 39-week envelope channels for the weekly S&P 500 index, we see a rally that continues to struggle at the upper channel bound which generally would be expected to limit the upside. Considering the high valuations of today’s equity averages, there is good reason to believe the current trend has run up against a resistance level as would be expected from prior history. Baring very unusual circumstances, I believe the upside resistance implied by this chart is a realistic conclusion of the current situation and a market top will be formed.

I should add that if this is true, one normally would expect the current rally to run out of steam within a few weeks, perhaps as a result of the very low mutual fund cash reserves noted in my last equity update, in the vicinity of the upper red dash line. The general intermediate conclusion would be that after the S&P 500 stalls at the upper red dash line, it would then turn down, perhaps dramatically, all the way to the black 39 week moving average that defines the center of the channel. Any test of the 39-week MA would normally provide a good rebound, back to the upper red envelope under these circumstances because the 39-week trend is up and this is a technical positive for any rebound historically. In any case we can address these projections after we get more trend data. Note the channel history in the 1999-2000 period.

Moving on to the Short Range T picture in the next daily chart we see a short term rebound has occurred since my last update. Click on chart for larger image.The key point is that the upside momentum is unlikely to break above of the green Cash Build Up line so no new T is likely at this time. In due course, probably by the end of this month or in March, a new oversold condition will set up a new T construction along the lines I have suggested in the daily chart. The most probable level at which this new rally might begin is the 55 day MA level noted in the chart. Because this MA is rising, the actual low is likely to be somewhat higher than the current price of the MA, but it is a good statistical estimate of the next key oversold condition level near the next Short Range T’s center post.

Nevertheless when this new T’s initial rally gets underway it is not likely to be able to sustain an uptrend throughout the very long right side of the new Short Range T. This is largely because the 39-week envelope picture will oppose such an advance. So this new T is more likely to collapse after its initial 2-4 week rally is over. It can however provide a very powerful short-range rally from the next oversold condition so there are at least some upside opportunities from the next oversold condition.

In summary, the near term outlook is to see the current rally fail, as it appears to be doing on Friday, then look for the next oversold condition as a potentially important low for a short term rally. This will probably take a few weeks. If the new T collapses after a good short term rally, as I expect, then the resulting decline can bring the S&P down to the lower 39 week MA for the next important low.

This lower low may not occur for a few months and perhaps not until Fall. …Terry Laundry.

Short Range T Update Feb 6 ’04

Short Range T Update for Friday February 6 2004

The Short Range T picture is unfolding normally in the chart below with the blue volume oscillator rebounding on Friday from a very oversold condition. Click on the image for a larger view.

It is too early to think about a new T because the market correction is too short time-wise and as a minimum a rally that fails is needed to set up the next T. In other words the current rally has limited upside potential and will likely fail in due course. The market would normally be expected to fall to new lows in a few weeks and at that time conditions for the formation of a new T would be much more likely. I think we have plenty of time to work out the details out this upcoming T, so I will delay some of the questions until another week or two has passed.

I was also interested in the Mutual Fund Cash Percent Assets chart above which was published at Jim Sinclair’s Web site over this weekend and shown here courtesy of its original source http://www.contraryinvestor.com also listed in my web sites below. I believe both these site are worth viewing and would check them out for “forward looking” views that I think have stood the test of time, but are often overlooked by trend following investors.

With respect to the new T that may have its center date low later this month there appears to be a problem with its prospective rally in the right side. I believe this very long time spanning T will require that we include the total (?-?-?) Cash Build-Up period as part of the time span within the left side of the next T. This will result in a very long spanning T that history suggests may not be able to sustain a market rally throughout its very long right side.

In T Theory any T that cannot support a price trend rally within its right side is term a “bearish type of T” and under adverse circumstances can allow a serious market decline to persist through most of its right side. The Mutual Fund Cash Percent Assets chart conclusions are particularly significant right now because it suggests that cash levels by this measure are at historic lows and cannot provide the fuel to maintain the long rally called for this T’s time nature.

Yet in a few weeks, an new, “yet to be seen”, over-sold condition should technically lead to a 2 to 3 week rebound rally that confirms the time span of a new T by breaking above the green down trend line in the blue volume oscillator. This next rally may last some 2-3 weeks and look strong for its short duration, however this rally should then fail quickly for lack of “real mutual fund cash”. In T Theory this new T should then collapse in the form of a bear type T since the long graphical representation of the Cash Build Up period has no basis in the real world of mutual fund cash (as Husk has commented). Later this year a new oversold condition should result.

Valuation Concepts

A Summary of Basic Valuation Concepts

In the past I have presented basic historical Price to Earnings Ratio Studies from the 1880 to present time in order to suggest that common stocks are over-priced. In this initial “typepad” discussion of this fundamentally important measure of earnings and equity value, I want to expand my discussion the three approaches that look worthwhile to me looking ahead for the next decade. I also want to comment on a new technical trend approach that may be promising and new Advance-Decline T research projects.

The three interesting fundamental approaches to equity valuations are:

A. The simple standard S&P Ratio definition which equals the current S&P 500 price divided by the last 12 months actual net earnings using standard accounting procedures.

B. The more sophisticated Dr. Robert Shiller P/E Ratio definition, which equals the current S&P 500 Price, divided by the 10-year average of these same standard earnings.

C. A more recent, and I think very innovative, Dr. John Hussman conceived P/E Ratio measure. Please read the web article provided in the web links at the lower left for details. Dr. Hussman defined the P/E Ratio as the current price of the S&P divided by the peak annual earnings seen over the last 10 years. This represents an optimistic measure of earnings and circumvents Wall Street’s arguments that P/E Ratios don’t matter when earning are depressed.

The whole point of these three defined measures is to help define the historical “fairness” at which an investor is buying earnings. When P/E ratios are high, as they are now, investors are paying a historic high price for a dollar of earnings. Buying high may work for the near term,

But the historic outlook for the longer term is for a proportionally poor rate of return. Historically buying when P/E Ratios are low has the opposite outcome; that is an above average rate of return is the more likely outcome if one buy low as defined by any of these P/E Ratios.

The problem with all these P/E Ratio concepts is that the current environment is being over ridden by the very low rates of interest as the Fed tries to halt a deflationary downward economic trend. Others have assumed that if the Fed prints money fast enough and in great enough quantity, then the high P/E Ratios normal historical negative connotations can be negated. I am very anxious to test this dubious claim. To do so, I am setting up an extensive database of monthly data.

It includes interest rates along with the usual earning, price and dividend info to get my T Theory interpretation working on “big picture” stuff. These amounts to a bit of work, so along the way, it pays to pick up a few other important technical ideas that could be tested very easily once the basic database has been set up. This will probably take a few months.

Michael Belkin has proposed an alternate technical criterion of the relative valuation of stocks. His moving average technique could make a valuable addition to the basic fundamental P/E ratio measure. It comes out of Michael Belkin’s very long-term technical work covering the last century so it overlaps the more fundamental P/E Ratio studies. He has proposed long-term technical trend measures that might represent an alternate view of over-valuations verses under-valuations. I have not had a chance to verify his claim that 200 week and 200 month moving averages can define key points over the last century but I can easily test it.

His trend technique makes use of unusually long term moving averages (MA), the 200-week MA and 200-month MA of stock indexes like the S&P 500 and NASDAQ index. Since I have the basic blue chip data needed to reproduce these moving averages in my database as part of the P/E ratio Studies, I can study Belkin’s historical conclusions and get a better idea of its validity relative to the conventional P/E Ratio studies that cover the same period.

In a October 2003 published review, Belkin contends that speculative bubbles can be identified by noting extreme upside deviations from the very slow moving 200 week MA, a 4 year MA. Like the Shiller interpretation, he reached the correct conclusion in 2000 for a NASDAQ bubble. Naturally I am anxious to see the 100-year history of his criteria and how it compares to Dr. Shiller’s interpretation of his high Price to 10-year Average Earnings valuation criteria. I do have monthly data for the Dow Industrial Average equivalents from 1800 and I can easily plot the 200-week MA as a monthly equivalent to his basic contention, then vary it to see how his criteria pans out over my 200 year database history.

On the downside, Belkin saw the NADAQ collapse after the 2000 bubble break as finding support at the 200 month MA (a 16.5 year MA). This level proved correct as support at the recent 2002 low. These criteria, if verified historically, would be interesting because none of the three P/E studies concluded an under-valuation low was seen a year ago.

Additionally, Belkin concluded in his October 2003 comments that a bear market recover would peak the NASDAQ near its 200-week MA (2280 at that time). If true, this still gives a little more room on the upside. This might depend on interest rates since there is some reason to believe that any increase in rates would be negative, but he was basically looking for an upside end to the current rally on any further strength.

More work needs to done in this area on my part before any definitive conclusions are justified. However the studies that I can make in my database, which include interest rate data, and P/E ratio data might shed additional light on this technical refinement. Since I already have the basic trend data for the blue chip averages, his interpretation can be verified by a fairly simple extension to my studies.

For this posting I just want to outline these key ideas to keep in mind while I set up the new research projects. As far as I am concerned, the fundamental measures of stock valuation presented by Shiller and Hussman are fine from a static view. They all conclude equities are grossly overvalued. But am also looking to include the more dynamic trend criteria that Belkin has noted for additional refinements.

To further complicate these long-term valuation issues I have also obtained, from a very personal and private friend, the daily Advance-Decline data from 1926 to the present. This is a difficult database to acquire but it is very important to the basic T Theory forecast, which can independently be derived from this Advance-Decline data. I am presently setting up this as a companion study to test A-D Ts from 1929 to the present. This will also become a topic here in a month or so.

A-D Ts have a long and reliable history as noted at my old web site and I am anxious to understand this much long history of the breadth index and how it interprets the current strength in the Advance-Decline line. My preliminary condition is the recent A-D Line strength is significant in terms of the long-range picture and it may provide downside support to the overvaluation conclusions expressed by Belkin and the three conventional P/E Ratio measures.

Nothing is certain as yet, but a long term trading range may be the logical outcome. …Terry Laundry

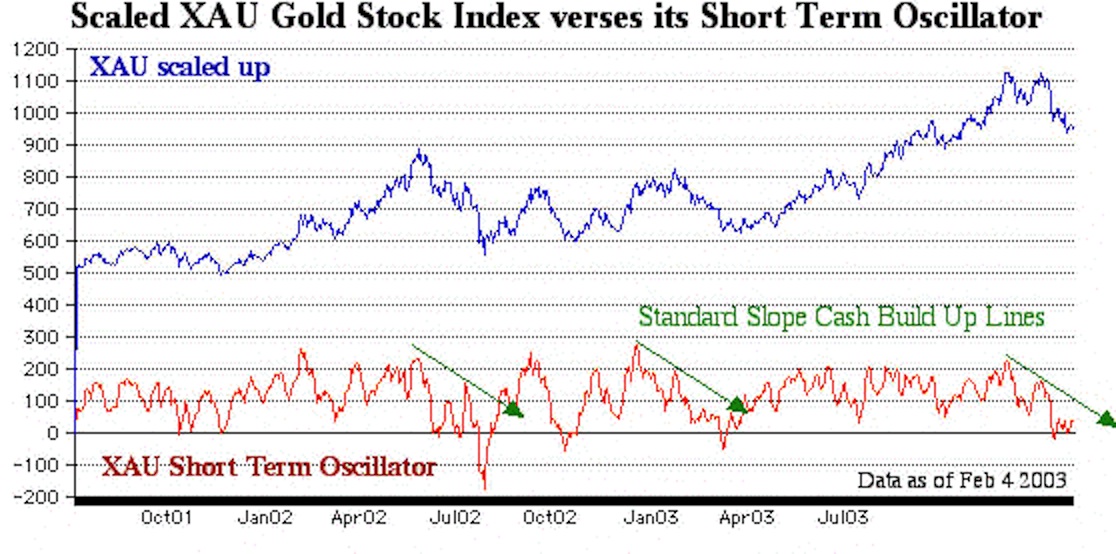

Short Range Gold XAU Update

The Short Range picture for the XAU Gold Stock index is shown in the chart below along with its price oscillator plotted in red. Click on the image for a larger picture of this important short term measure. The main point is to see if the green Cash Build Up Line can be broken to the upside signaling a new rally is getting under way.

I would wait a bit here because the Gold Community is skitish and the more ideal low could come after one more short term drop to a more significant over sold condition. To be continued.

****************************************************************************************

All Rights Reserved By The T Theory® Foundation ©

Order the T Theory® Encyclopedia

For a complete understanding of the T Theory® and how to successfully use Terry’s unique methods, order the Encyclopedia from Paula at the above link. There is additional material in the encyclopedia not covered here. Paula will be more than happy to answer your questions too.

Many thanks to Paula Burke for her permission to re-post Terry’s old T Theory® explanations. The period re-blogged on these pages are some of Terry Laundry’s best work and was published here from public domain.

****************************************************************************************

I claim no credit for the material found under T Theory® on this blog. All of this material is the creation of Terry Laundry and was downloaded from Terry’s free blog site (TypePad). I have created a mirror of Terry’s original material and now there is a second site containing Terry’s T Theory®. One or both of these websites hopefully will survive through time as Terry’s material is too important to be lost to the ravages of time. This site is simply a memorial to his lifetime work.

The page content re-blogged here is exactly as Terry created on his original webpages (saved on my computer with ScrapBook)). Nothing has been left out from the period Dec 2003 to June 2011. From Terry’s site, I made a lot of formatting changes, creating a more easily readable webpage appearance. The PDF chart duplicates of the JPEGs have been omitted for ease and speed of recreating Terry’s pages. References to PDF charts should be ignored (but no chart was left out).

After June 2011, Terry created a paid subscription website. None of that material is found here.

There were many many, many hours spent on this project; downloading Terry’s individual charts & audio files, followed by the uploading of Terry’s charts and audio to my WordPress blog library, after which I had to insert the uploaded material into my new T Theory® webpages (hopefully in the correct places). This was a dull and arduous project and I hope you enjoy it. I don’t believe there remains any more of Terry’s material in free domain, so my T Theory® project is probably finished. If I’ve missed something, you can leave me a comment.

If you find an uploaded reference error (chart or audio in the wrong place), please note the month and year of the webpage, plus the exact name of the referenced error file. Include any other info that will help me locate the problem file and where it occurs on the webpage. Leave a comment for me with the info and I’ll fix it.

Terry’s material is very long and will take many weeks for you to finish. Don’t hurry, it’s not a marathon and you will absorb more if you go through it at a reasonable rate. This is especially true for those who don’t invest in the T Theory® reference encyclopedia. The encyclopedia is a written reference for T Theory® and includes everything of importance for Terry’s T Theory®. Without the reference encyclopedia you must depend on your memory and Terry’s method carries some rules that you could easily violate. The encyclopedia also includes new information never seen on his website.

You are welcome to save any or all of my blog material to your computer. You also have my permission to re-blog my information, but you must (1) credit me and my blog in an obvious manner and (2) don’t change my material.

FYI – I find the best way to save a webpage is using “ScrapBook” (it’s an add-on for the FireFox browser). ScrapBook saves a webpage to your computer EXACTLY as it appears on the day you saved it. You can’t tell the difference between the internet webpage and your ScrapBook saved webpage. The saved pages are not pictures. Instead the pages consist of HTML and page functionality remains identical on your computer. There is also a second method for using ScrapBook, where you can save all of the webpages down to a defined link depth. This optional method means all links will function on your computer to the link depth specified (meaning you can click on links on your saved webpages and tunnel down into pages within pages). Saving the normal way will only save the top webpage but the links that exist could continue to function by taking you to the website on the internet instead of on your computer. But sometimes the linked website doesn’t exist anymore. I’ve had this happen on some very good webpages with unique information (they just disappear into the internet void). That’s a bummer when you lost some really good info and thus rose my need for ScrapBook. You can also filter the pages saved using the optional ScrapBook method, which can exclude all pages not coming directly from the specified website (filtering is recommended using this method otherwise you wind up with a LOT of useless stuff).

.

Explore posts in the same categories: . . . T Theory®

April 17, 2013 at 4:11 PM

I have no control over the blog’s emails. It’s an automatic function as I post a new update.

Just ignore and delete them.

I deleted all of your personal info in your comment as it was visible to everyone that looks at the blog’s comments. I didn’t think you would want that out for public consumption.

Bob

LikeLike

April 17, 2013 at 4:04 PM

Stop sending me this stuff

Steven Glenn

LikeLike