Death Of a Gunslinger – 1955 to 1987

There is a LOT of growing into a gunslinger that takes place in this story until in one stroke came disaster. It was a precursor to the 1987 meltdown. An event that I was not a participant, thankfully.

It’s a fun read and there are great lessons to be learned. So read on about the evolution and tales of Gunslinger Bob.

BUT FIRST . . .

Gunslinger Bob knows old traders and he knows bold traders . . . but he knows no old and bold traders!

Most of you won’t take the time to absorb the above phrase. Think about it while you decide to be a hair on fire gunslinger or an average speculating investor.

I spent all of my life studying market direction. I held the theory from an early age that on occasion:

It can be more important WHEN you buy or sell, than WHAT you buy or sell.

Regardless of investment quality, I didn’t like holding stocks during a bear market because everything went down during the bear cycle. Buy and hold investors give back a substantial part of their bull market winnings as the Bear invades everyone’s satchel of money. I was too greedy to knowingly let this happen. So I looked for the unobtainable and impossible secret to the stock market. Thus begins the trip into the future, first becoming a gunslinger and then content to be a speculator whose hair wasn’t on fire.

When I say bear market, I’m referring to a significant decline that lasts about a year or longer. The length of time of the corrective process is a significant component of a bear market. All other declines are corrections in an ongoing bull market. Hey, that’s important, write that down cuz we’re going to have a test later.

Unfortunately, the ability to predict a bear or bull market would see a lot of years pass before I knew a major market turning point was coming. That means lotsa dollars said goodbye on their way into other hands from my vulnerable savings.

The beginning of my stock market learning process started in 1955 as I questioned my grandfather about his investments in utility stocks for their dividends. He gave me my start on understanding how the investment process worked. I saw him lose money chasing dividends and I found that bothersome. Often times a high dividend company would not be able to support its high dividend payout and would cut their dividend, which in turn would cause the stock to tumble. As I saw this take place occasionally to my grandfather, I vowed to never chase a dividend that didn’t have the fundamentals to support the payout.

About this time I wished I had read an old book entitled “One Way Pockets” published in 1917. But I was so dumb to not recognize that there was pure gold in some of those old books and this was one of them. Here are some of the outlined nuggets from this old and highly recommended book. Everyone should have a copy in their library. It’s available on Amazon.

ONE WAY POCKETS

The following are condensed excerpts from the book, “One-Way Pockets”.

The start of a bull move begins in two ways

BUY after a protracted period of dullness and narrow fluctuations, the market breaks through the trading area with increased volume on the advance. The reverse is true for shorting.

BUY after a period of declining prices or dullness, or the market advances or refuses to go down following BAD NEWS. The market should absorb the news for an entire day and should be bought only after the market advances above the point where the news was received.

What to buy

Two or three active stocks is recommended but don’t pick the ones that have shown the greatest weakness. The issues to select are the active ones that have declined the least.

News

Stocks sold on news will bring the lowest prices of the day because each seller is competing with other sellers who have learned the news at the same time.

Stop orders

Place your stop order one point below the low that occurred at the bottom of the latest range and the reverse is true for shorts. A stop order will prevent a poor guess from turning into a serious loss.

First correction

Don’t make the mistake of trying to anticipate the top no matter how firmly you believe that the advance has gone “too fast” or “too far”.

It’ s at this stage of a bull market that those who have guessed right on the trend try to trade the secondary reaction. Don’t short sell at this stage of the advance and don’t sell long stock.

This correction is not likely to wipe out more than half of the previous advance. Your position should be strong enough to increase your commitment when the market shows the first sign of resistance on the downside.

The correction may catch the stop loss orders placed by traders a few points under the top. Having done this, it usually rallies so quickly that the traders have no opportunity to buy back in except at higher prices.

The first selling point

Because it’s impossible to determine whether the market is going higher, you should sell on the recovery to the former high. The stock should be bought on the correction and kept until the trend is clear.

The process of increasing your position on the corrections and decreasing it on the recoveries should be repeated as long as the market continues to advance into new high territory.

The great distribution

The time will come when instead of resuming the advance stocks will mark time in the vicinity of the previous top. The old leaders will be replaced and give the unwary speculator the impression that the bull-move has resumed. Stocks that are being distributed will have sharp but short-lived advances followed by a gradual decline. The entire market will have a highly irregular appearance. Before this stage is reached the market usually has several successive days in which the volume is very high with intense speculative excitement.

The topping action is similar to that displayed on several other occasions but the public is now a large buyer. Their orders are placed in active stocks several points below the top and the demand moves the market back and forth within a trading range. This is the great distribution stage. Its duration depends upon the extent of the previous advance, the volume being offered for sale and the buying capacity of the public.

When these symptoms are observed and the market fails to advance to new

ground, sell all stocks. Not only is this the time to sell long stock but it is also the time to open a position in shorts.

Covering shorts too soon

Short that are placed early in a bear market are invariably covered too soon and resold at lower prices. It’ s the same as long stock bought at the start of a rising market that is quickly sold and later repurchased at higher prices.

Cover your shorts when the market no longer goes down on bad news or when it moves up through a trading area as described in the start of a bull movement.

In 1955 computers were machines that filled a refrigerated room and only the government could afford to buy one. It would be another 22 years before I had my first computer (1977) and could chart and study stocks by machine. One important point regarding charting stocks by computer, it will cause you to lose an edge that can only be found charting by hand. Try charting by hand for at least 6 months and see if you can tell the difference. You’ll find that you’ll get in sync with the stock as you chart by hand. I found myself getting in the groove with the stock or overall market as I charted by hand. Many times I felt I’ve left some good practices behind me. I’ve looked back at some of my writing from the 1970s and 1980s and wondered, “That’s really good. How did I do that”???

In 1955 I was too young to have my own brokerage account and I had very little money. I was a typical broke 14 year old kid, but I had some crazy ideas about the stock market. I convinced my father to open a brokerage account and I pooled my money with him. After I did the research on a group of stocks, my father would agree with my suggestion to buy a particular stock. The stocks we bought were usually high flyers with lotsa followers, think of the FAANG stocks of today only we called them “glamor” stocks back then. The high flyers drove my father batty because of their high volatility. He liked it when the stock went up, but caused him too much anxiety when the stock corrected. From prior observations, I knew that stocks that went up 7-10 points in one day were going to lose a big chunk of that back sooner or later. I understood all about zig zag as a normal stock market process (observations taught me normal movement). One stock we owned was Lukens Steel (imagine a steel stock as a high flyer, different times folks). It had a strong uninterrupted run over many days of sizable upside points, and then it lost a big part of that gain all in one day (17 points). My father thought the world had ended and he sold. Lukens Steel subsequently soared far above his sell point and was a source of irritation for me. We left a LOT of money on the table.

In these early days I would take a trip to our nearest office for Merrill Lynch Pierce Fenner and Beane. Yup, there was a Beane at the end of their name when I started my stock market education, but it changed in the 1950s from Beane to Smith. I went to their office a few times and they had a wall of electro mechanical price dials that were spinning by solenoid activation. At the top of the high, low, last price dials would be the symbol for the stock represented. These devices were really noisy and were constantly clattering as prices changed. Down the block was EF Hutton, considered to be a more upscale operation. In those days one million shares in a single day was a big deal and the stock market was also open on Saturday during the 1950s. Things have changed a bit since then. Ya think???

After Lukens Steel I was convinced that I had to control my own brokerage account. I saved all my money from my first real job (Jack in the Box). My father opened another brokerage account (still in his name because I wasn’t legal age), but I had complete authority over this account (my money, my account). This account had only my money and it was mine to make or break. This was the real beginning of my investing career.

In the fall of 1957, the first stock I bought for “my” account was Ampex (they invented the video tape recorder). I bought it after it had gone up a bunch, split and I paid $44/share. It promptly went down to $40 and sat there for several months. What a dud. It just sat there stagnant plus I had a small loss. Did I do something wrong??? Then one day for no particular reason it jumped several points, did nothing for a couple of days and then jumped again. This trend kept up for months. Naturally there were the normal zig zags, but before long Ampex was going parabolic. I sold it in the first half of 1958 at $120 and bought my first car. Hot stuff, I’m 16 years old and I bought a 1 year old car and paid cash. Ampex kept soaring and splitting, but I was happy with my car. I was greedy but practical.

WOW! Making money in the stock market. This is so easy.

I was thinking, why should I ever work again??? I can buy and sell stocks the rest of my life and before long I’ll have more money than I know what to do with. Why aren’t more people doing this? I guess they just didn’t have my “talent”. Yeah, I had the Midas touch.

I had just committed one of the GREAT CARDINAL SINS of Wall Street:

“NEVER CONFUSE GENIUS WITH A BULL MARKET”.

It’s very easy to confuse genius with a bull market. I personally knew a lot of geniuses during the late 1990s. They all thought I was nuts warning them about an ending to the 1990s bull market. They knew far more than I did, because they were stock market geniuses and I wasn’t. Yup, it’s real easy to fall into that trap. Been there, done that. By the 1990s I had been around the block many times and knew that stocks don’t reach for the sky forever. Knowledge is a scary thing as it makes you keep your feet on the ground, while those around you (new gunslingers) are making too much money without any fear. NO FEAR can be a precious thing during the latter stages of a bull market. No fear will allow you to be part of the crazyiness of the stock market without any thought to an ending coming that will snatch your money away in a heartbeat.

Meanwhile back to my teen years, I did learn that there was a downside to stock market investing. I wasn’t a stock market genius anymore, I had just been lucky and now reality was hitting home. The bull market had hit the pause button and I wasn’t told about it.

In later years as I gained more knowledge about the stock market, I developed a few rules. I was still a trend follower (aka member of the crowd), but I had some discipline.

My stock selection was pretty simple, I would buy a stock with high growth prospects (usually a company with little competition and a great product. After the 1973-1974 bear market I bought Pall Corp (filters) and Tandy (Radio Shack as they became known). I looked for sponsorship (persistent buying volume) as this was an important component of my stock selection. I would hold the stock as long as the growth prospects remained intact and the company’s price and volume showed continuing sponsorship. I favored a stock that could stop its correction by only penetrating a small distance into its prior peak. I watched my stocks (lotsa eggs in only a couple of baskets) very closely and usually knew when it was acting right or wrong. I always charted the stock’s daily price and volume by hand.

From 1957 to the early 1970s, I used stock selection as my stock market investing technique. During this period Standard & Poors had a “monthly stock guide” (blue pages and blue gray cover). I used this booklet to scan for stocks with good fundamentals and were on the move to the upside. This was simply finding a stock with good fundamental prospects PLUS it had to have sponsorship, meaning there were people or institutions that were buying the stock. I abhorred the prospect of buying a great fundamentally sound stock to see it sit and do nothing. That’s not the name of the game. Waiting was wasting my time and money.

Margin pyramiding is a strategy that can only be used successfully when “It was the best of times, it was the worst of times”. (borrowed that one from Chuck)

If you are unfamiliar with the term, margin pyramiding, hopefully, the following example can clear the fog.

A margin pyramiding strategy is an investment approach with higher risk, but with proper money management it can produce great results.

For example: During 2008, the market collapsed with only a few small upward corrections. If a trader was short in this type of market environment, it would be a prime candidate for margin pyramiding. In the below chart, Citigroup took a beating during 2008. In a pyramiding strategy, the trader would add to their short positions on each upward bounce using the paper profits in their margin account. Paper profits exist as real money in your margin account (ask your broker). This process of adding to your short position with your paper profits would have continued down to the bottom in March 2009. The end result is this would have produced much greater returns than simply shorting the stock at the peak and riding it down in a single trade. Simpler that way but doesn’t maximize your position.

The only problem with using this technique is that it raises the level where you can receive a margin call. But I’ve used this technique for years without a margin call. Picking the right stock and the right timing is extremely important, otherwise, you could easily be in trouble.

Margin pyramiding can be used in a bull market in the opposite manner described above. Margin pyramiding was my first introduction to higher leverage than conventional margin. I don’t remember the year that I first used this technique.

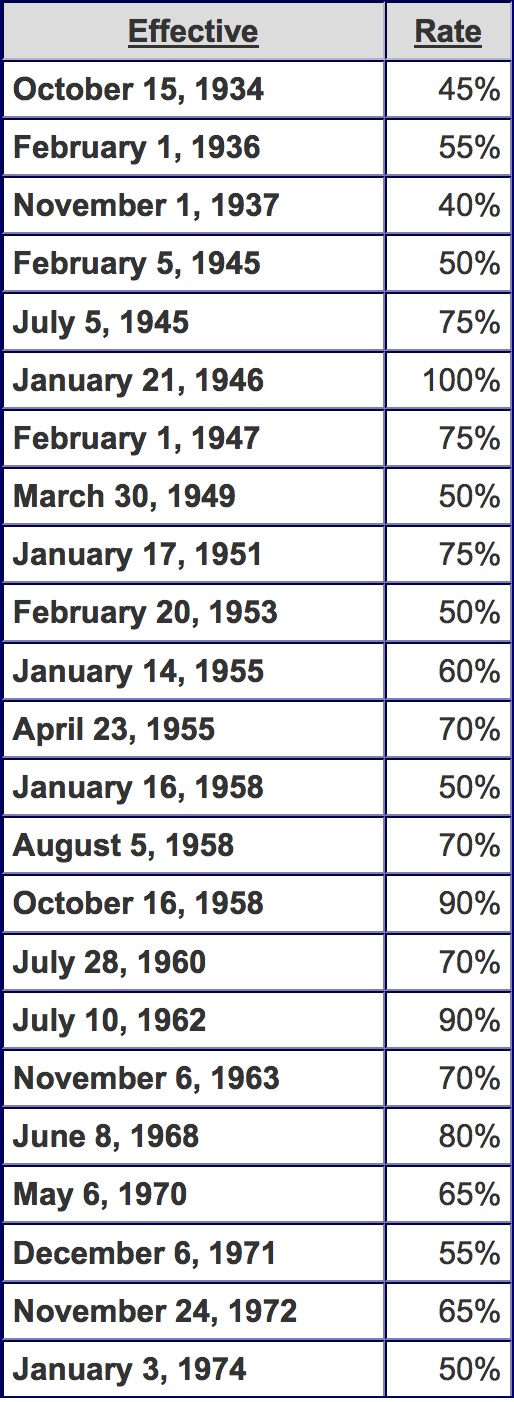

When I began investing in the market, the margin was 70% and it has fluctuated considerably through the years. It’s been unchanged at 50% since 1974. Looking at the margin rates and dates below, the present 50% rate has been unchanged for over 40 years. Prior to 1974, margin rates had been changed every couple of years.

The FED used margin rates to slow or accelerate the stock market. They’ve steered clear of this method for a long time now.

Before the early 1970s, there were no exotic stock market products, such as index mutual funds, index ETFs or stock market index futures and their options. There were individual stocks and that was it. Options existed but were Over The Counter (OTC, precursor to the NASDAQ) and had no uniform pricing or strikes. Real option trading didn’t exist until the formation of the CBOE (Jan 1, 1973). This was the beginning of the NYSE and imagination. A plethora of products came in the later decades.

During the mid-1970s to late 1970s, I was a subscriber to Edson Gould’s “Findings & Forecasts”. Many thanks to Edson Gould for teaching me perspective and the importance of studying the psychology of people and the “crowd”.

Before Edson Gould’s teaching, it was a long and sometimes tortuous learning process for me. When the learning process was painful, I always asked myself, what did I do wrong, and what can I do to correct this mistake and not repeat it. Reflection taught me humility (which sadly I lost for awhile during the 1980s, more later).

During the early 1970s, I read an article (Time magazine??) about the Coral Index based in London. Coral was a gambling establishment that was taking bets on the direction of the Dow Jones Industrials. Hmmmm, this seemed like something I might want to try.

The following is not the initial article I read, but it gives you a general sense of the Coral Index. There are a few errors in this article.

Click to enlarge

The next article explains that the maximum bet was 1,000 pounds and makes a few items clearer.

Coral Index article from the New York Times, February 18, 1978

LONDON BOOKIES TAKE ON STOCK MARKET, The New York Times News Service, LONDON — It is one of the most frustrating things in the stock market, you “know” it’s going up, but you don’t buy because it would be just your luck to pick the one stock in 20 that would head straight down.

You will have called the market right again — and still not be making money Well, there’s help for you. A small, little-known company takes bets on which way the Dow Jones industrial average will move. No more risks of buying Penn Central or Equity Funding. No more commissions or advisory fees to pay. No more tying up all your capital. All you have to do is pick up the phone, dial 011-44-1493-5261, and ask for Christopher Hales, the stock market’s Jimmy the Greek. Hales and his two associates here are market bookies, employing the point spread and their wits against the punters of the world. “It’s a gamble — you can’t get away from that”, said Hales, a 38-year-old former stock market and commodities operator, who looks as if he would be as much at home in the lofty reaches of the Bank of England.

Here is how it works. You buy or sell “lumps” of the Dow Industrials, composed of 30 leading issues on the New York stock Exchange. The minimum is two one-pound units ($3.90) and the maximum is 1,000 units ($1,950). If you buy and the market goes up, you will probably make money. You will also win if you sell and the market falls. Like all businesses, Hales’s company, Coral Index Ltd, needs a profit margin. It creates this by making a 10-point spread between its buying and selling prices, usually straddling the current level.

Last Friday, Jan 27, for example, the Dow closed at 764 12. Coral opened its quotes Jan 30 at 760 for sellers, 770 for buyers. If you bought, say, 10 units at 770 and the index jumps to 810 you would make 40 x 10 pounds, or 80 pounds. You don’t have long, however, to be right. No bets last more than 30 days “We reckon the Dow won’t often move more than 50 points in a month.” says Hales, noting that the relatively short period tends to keep its own and customers’ losses from getting out of hand. It also allows Coral to keep slicing away with the spread though Hales insists this is not the biggest factor in its profits. “What we’re really relying on is that the average investor is going to be more wrong than right.” The spread helps us to balance the book and gives us enough to cover the overhead.

All transactions are made by phone; the mail is considered too slow, too unreliable and in some places of dubious legality. About half of Coral’s business is in the Dow Industrials, with the rest in the Financial Times of London’s industrial ordinary index of 30 British stocks. The spread for the London market is five points because of its lower level.

Coral, operating from a second-story office on fashionable Berkeley Square, began taking bets on the Financial Times index in 1964, adding the Dow in 1967. It didn’t attract much interest, however, until the 1970s. and even now only about 100 customers of the 6,000 are Americans, many living overseas. Most customers are brokers or others with close ties to the market, some hedging positions in options or stocks. Swiss money managers are frequent players.

(Bob’s note: I didn’t realize that I was only 1 of 100 people in the USA that was dealing with the Coral Index. I only realized this when I found this article. I did know that I had achieved a bit of notoriety at Coral as I was an infrequent bettor (once every few months) and was always betting in the opposite direction of the crowd, plus I never lost a bet.)

Coral says: There are also nonprofessional bettors in the United States, Europe, and Australia. If you are a really high roller, say $40 a point and up. you can telephone Coral collect. You can also haggle about the price. Although the company does not guarantee to take more than 100 units, you can probably negotiate higher stakes, perhaps at a higher spread. Hales says there are a few people who win consistently. They are not particularly unwelcome, he says, since they help Coral adjust the spread, which in a volatile market may change 20 or 30 times a day. One reason Coral thinks most bettors will be wrong is that they are usually playing with their own money and thus tend to make mistakes under stress; the “house.” using corporate funds, can remain calm.

In the early days. Coral would often partly hedge its position by buying or selling some shares. But it couldn’t improve its performance this way and now unlike most bookies it does not lay off any of its risks. “We don’t hedge anything, ever,” Hales says.

Sometime in the late 1970s (I forget the exact year), I opened an account with Coral Index and began betting on the direction of the Dow Jones Industrials.

I would call London several hours before the New York Stock Exchange opened (calling usually around 3 AM Pacific time) and place my bet. I spent a lot of time with no bet, waiting for the market to be on the edge of a turn, up or down. I never made a bet unless I thought a market turn was imminent and probably significant. I spent a great deal of the time without a bet, but that was fine because winning a bet had a high rate of return.

It was kinda funny when I called to place my bet because there would always be a flood of bets going in the opposite direction of my bet. This helped me considerably because I would be given a very favorable spread in the event of a market reversal. My positive spread was due to heavy betting pressure by the crowd in the opposite direction of my bet. The spread always follows the crowd and keeps it harder for them to win.

During a quickly declining market, Coral would create a spread that was heavily biased to the downside. This is how the house tried to put the odds in their favor. Without a favorable spread for the house, Coral could be out of business. Due to the high negative spread, the market had to fall a fair distance before your short side bet would be profitable. But if you placed a long side bet during a high negative spread situation and a reversal took place, your profits were instantaneous and greater than normal. Big rush when that happened and that was frequently the situation I faced, the crowd going in one direction and I was going the other way.

For instance: If the Dow Industrials traded presently at 850 and had been falling steadily with increasingly heavier downward pressure, you would receive a price around 830 for a short and 840 for a long. Playing for the reversal, I would buy a long at 840. If the market rallied 20 points over the next week to 870, my profit wasn’t 20 points. It would be 30 points (870 – 840 = 30). This was because I received a 10-point discount from the prior close when I placed my long side bet. That gives you an idea of how the spread pressure would work in my favor.

I remember one occasion in particular when I had bet long and received a very high 20-point discount from the prior day’s close. This was due to huge downside selling pressure. Remember during this period, the Dow Industrials price level was always less than 1,000, averaging around 800-850. 20 points at that time represented over 700 points in today’s market.

In many ways, the Coral bets had the same significant problems of an option, TIME and PRICE. Time was constantly your enemy because the bet only lasted 30 days. You only had 30 days to overcome the spread. For this reason, I would only bet when there was a significant chance of a reversal. Because of the time factor, my money usually was sitting in a bank in London when I had no bet.

I never had a loss during my time with Coral and this had been noted by the people that I dealt with at Coral. I was always taking an opposite position against the present market trend and this made me an unusual client at Coral. Along the way, I had some interesting conversations with Coral.

But things changed when another opportunity arose. In 1981 the Kansas City Board of Trade introduced trading in a stock index futures contract based on the Value Line Index. The leverage was quite high and the initial margin was low. This was the first stock market commodity index future. I could see a new opportunity opening for me. I brought my money back to the USA from London and opened a commodity account. I had sworn years earlier that I would never have a commodity account and here I am going against a strategy that I said I would never use. HEY . . . I know what I’m doing!!! GULP.

The following article is from the New York Times, March 26, 1982.

“COMMODITIES; Linking Dow Average to Value Line Futures

By H. J. Maidenberg

Published: March 26, 1982

The new stock-index futures based on the Value Line average followed the overall price trend in the stock market yesterday by advancing 60 to 65 points, or $300 to $325 on a contract, with the active near-June delivery closing at 124.65, for a gain of 60 points on the day. (Bob’s note: a point is a penny and the leverage is $5 per penny).

Indeed, since the first stock-index futures began trading on the Kansas City Board of Trade last Feb. 24, contract prices have mirrored not only the Value Line average of 1,683 stocks, but also the ups and downs of the market.

”Our index futures are now being accepted as a true measure of market sentiment,” said Loren A. Brown Jr., a broker member of the exchange and head of the committee that fashioned the new investment instrument, ”now that many traders think they have discovered the price ratio between the Dow Jones industrial average and the Value Line.”

According to Mr. Brown, the generally accepted rule of thumb that is being used is a ratio of about 7 to 1; that is, each 100 points, or $1, move on the Value Line is equivalent to a $7 move on the Dow. Yesterday, the Dow Jones industrial average of 30 shares closed up $4.29, which is seven times greater than the 60-point gain on the active June Value Line futures.

How the Averages Differ:

One major difference between the two averages is that the Value Line average figures are calculated by a mathematical formula, while the Dow Jones average represents the dollar value of the 30 shares, adjusted for stock splits and related changes in prices.

Further, the futures price of the index is not necessarily the same as the Value Line average, compiled by Arnold Bernhard & Company. For example, an officer of the company noted that the average closed at 125.91, up 55 cents on the day, compared with the spot March futures, which ended at 125.65. The prices of the Value Line futures are determined in the trading pit of the Kansas City exchange.

But the Dow-Value Line ratio is deemed important because most traders have been accustomed to relying on the Dow Jones average as a convenient barometer of market sentiment, and some thought that investors would find it difficult to adjust their thinking to the much broader average. But the open interest, or the number of contracts that are open for trading, has grown steadily.

As of Wednesday’s close, the open interest had grown to 3,302 contracts. Yesterday’s figures will be released this morning, as is the practice on all commodity exchanges. Recent volume has averaged 1,900 contracts a session. This activity compares favorably with financial futures in their first month of trading.

Specifically, each index contract consists of the 1,683 stocks in the Value Line index multiplied by 500. Thus, the June futures contract, which closed yesterday at 124.65, works out to a value of $62,355 in stock. Each one point move in the Value Line index was a move of $500 in my equity. Initial cash margins for speculators, or non-trade hedgers, had been set at $6,500 (about 10% margin).

Also, the stock-index futures are settled by cash on the last trading day of the delivery month. This means that buyers do not take physical delivery at expiration time, nor must those who have sold short come up with any shares.”

I traded the Kansas City contracts for a little more than one year. But the handwriting was on the wall. The CME had introduced a futures contract based on the S&P 500 index. The CME had a broader appeal and their contracts surged in popularity displaying excellent liquidity. The CME was the big leagues compared to Kansas City.

The original SP 500 contracts were equal to 10 mini contracts (a mini contract is today’s norm).f The leverage was $500 per S&P 500 point for the original contracts. A mini contract is equal to $50 per S&P point. I made the shift from the Kansas City contracts to the S&P 500 contracts ($500 per point) as it became obvious that liquidity was much greater at the CME. With higher liquidity, market orders were executed very quickly with smaller deviations from the quoted price.

To this day I’m still trading the S&P 500 futures contracts ($50 per point), but my use of leverage is much lower after peaking at a VERY ABSURD level in 1987. I guess I’ve grown conservative in my old age and the gunslinger has also gotten smarter along the way. Just remember that with high leverage, you make a lot of money when correct and you lose a lot of money when you’re wrong.

The large S&P 500 Contract ($500 per point) is still traded, but only during CME’s regular hours and it is pit traded with open outcry. The CME mini contract ($50 per point) is traded nearly 24 hours per day except Saturday and a shortened day on Sunday. It is electronically traded and during after hours of the CME, there are no market trades, only Limit or Stop prices. BUT a Stop order does become a market order in after hours trading. This is the only way a market trade can be made after hours.

Want to hear a crazy day of pit trading in the S&P futures. This is the Flash Crash of 2010 where the market lost 1,000 DJIA points in minutes and then began recovering. It is WILD!!!!

Hope you watched the video cuz it’s the wildest you’ll likely ever hear or see.

Everyone should always use Stops to control their losses while trading the S&P 500 futures contracts. Some traders use mental stops, but the problem with mental stops is that the trader is likely to rationalize that the position is correct and it’s going to turn around very shortly. The situation usually only gets worse. I’ve never used mental stops, preferring the hard stop instead.

Stops should be placed carefully. You need to figure out what shouldn’t happen if your position is correct. At what specific point has your position gone wrong (breaking of support or resistance levels)??? Place your stop a bit beyond that point. This requires some thought to arrive at the right stop level. The stop should be entered immediately after your position is established.

I don’t believe in setting stops at a certain percentage above or below your position. That’s an arbitrary level and means you aren’t doing your homework. I believe that stops should be based on the penetration of a significant high or low that wouldn’t take place if your position is correct. Your position ideally should be established reasonably close to your stop so your loss is easily tolerable if you’re wrong.

If you don’t use stops, you could freeze up and never liquidate your position until you have the forced margin call. Even worse is the unattended position. Somebody gets busy and forgets to watch their investment. When they remember to look they may be pleasantly surprised at how much money they’ve made, but what if they find they’ve lost a huge chunk of their account. It happens.

I urge those who are new to commodity contract trading to limit their trading to one contract for a considerable length of time. It’s your learning experience at futures school and your learning isn’t complete until you’ve encountered all types of markets and market surprises, specifically a bear market. A bear market may take you out and beat the hell out of you before you realize that you are in a bear market. Surviving and making money is always the name of the game.

My investing experiences began with speculative investing. Evolved into position trading in the Dow Jones Industrials, the Value Line Index, and then the SP 500 index (individual stocks, Coral Index, Kansas City Value Line, and now the CME SP 500).

So now we’re in the early 1980s and I’ve been tutored by the best technician of the 20th century (Edson Gould) and I’m no longer investing in individual stocks but commodity contracts that represent the entire market. The leverage in these commodity contracts is VERY HIGH and profits make them very alluring. Losses, what losses. My crazy trip is nothing but HUGE successes until . . . something went wrong.

In August of 1982 I anticipated a turn upward in the stock market after falling since its peak in 1981. At this time Wall Street is deep in an emotional depression and can’t see any reason why the market should rally. Wall Street hasn’t come to grips with the fact that FED Chairman Volcker has almost single handed broken the back of inflation (causing 10% unemployment). Soon a wild rally in bonds will begin as interest rates plummet for the next 40 years. Reagan is President and the nation will soon believe in itself again.

I bought a few Kansas City contracts on Wednesday, August 4, 1982 as I had detected a bottom in the market. But the market continued on down on Thursday and Friday. My wife and I went out to dinner that Friday night and I explained to her that I’m getting killed by the leverage as the market hasn’t turned up as anticipated. We decide to see what happens on Monday as I reassured her that my secret indicator turned up on Wednesday. On Monday, August 9, 1982, the fuse was lit for the stock market rocket and off it went, immediately wiping out my losses and putting me solidly into a profitable position on the first day of the bull market. August of 1982 was the birth of the 18-year bull market that didn’t end until 2000.

I was on a roll and making a LOT of money. Beginning in 1982 I began increasing my use of leverage and bought more and more futures contracts. My leverage was enormous by 1987 (absurdly enormous). As we approached 1987 I had suffered NO LOSSES in several years (true story) and had nothing but hugely profitable trades. Profits of $50,000 or more per day were not unusual and am I getting a swelled head because I was raking in lotsa gold every week. I’m trading the market profitably in both directions, long and short. WOW, finally I’m going to retire as I had dreamed as a teenager and never work again!!!

And then . . . September 1987 hit and something went wrong with my secret indicator. Actually, I was not interpreting it correctly as the indicator had transitioned and needed an adjustment in my interpretation (my arrogance of success blinded me). By October 4, 1987, I threw in the towel and bailed on the contracts as I had incurred a stratospheric loss of all of my capital due to very high leverage in the wrong direction. I was out and sitting on the sidelines when the October 19, 1987 crash occurred (Black Monday, Dow Jones Industrials lost almost 23% in one day). If I had been on the wrong side of the market on that day, I would have been totally bankrupt, losing everything, house, businesses, etc. But I sat quietly on the sidelines watching despair and grief overtake Wall Street.

The precursor to CNBC was FNN, Financial News Network. I watched the crash unfold on FNN as they interviewed people in New York and Chicago. I have some of the FNN comments on my YouTube channel. I saw a WELL KNOWN but now retired cycles analyst say on October 19, 1987, “Sell everything”

Many dealers, traders and brokerages were wiped out on that day. Greenspan and the FED rescued brokerages that had been taken down by their customers not meeting margin calls.

FNN in later years was swallowed up by CNBC. Bill Griffeth and Sue Herera were anchors from FNN and years later still on CNBC.

What did I learn from this horrible incident? (1) My gunslingers days were finished, I now became a more moderate low leveraged investor, and (2) ARROGANCE KILLS . . . and my arrogance had nearly made me into a pauper. My arrogance was derived from the fact that I’d forgotten what it was like to take a loss. Constant winning is not the norm and someday the market will catch you sleeping and kill you. Thus began an abrupt change in my speculative life. After 1987 when I felt like coming back into the market (it literally took years fro me to come back as I had been gutted) I reduced my contract leverage to only one contract as I tried to rebuild my savings (still haven’t hit the 1987 high point and never will). To this day I usually only trade one contract because I have such a bitter taste of going bankrupt. Immediately after 1987, I felt like Steve McQueen in The Cincinnati Kid, where Cincinnati Kid didn’t think he would ever win again. But slowly I let the demons of the past die and moved on to a more normal speculative attitude. No more running around with my hair on fire, I just took it easier and was thankful another day was still left for me.

My knowledge didn’t die in September 1987 although I look back on some of my writings during the 1980s and wonder HOW DID I DO THAT??? Obviously I have left some of my knowledge in the past, not intentionally but by an accident of time and non-use during the intervening years of a forced retirement from the market. It took me quite awhile to feel like investing in the market again.

After facing nearly the loss of all my capital, I changed my attitude to a more reasonable approach to the market. I’ve continued to expand on my knowledge of the market but as I said before stopping hand charting leaves something behind that will be missed. You linger longer when you are hand charting and become more thoughtful and less likely to miss something. In the old days I was out in front of the market where today, I let the market tell me what is happening as we approach a turn.

In finality, never again would I abuse leverage.

I know old traders and I know bold traders . . . but I know no old and bold traders!

September 1987 was the end of the beginning and the start of the rest of my conservative but still speculative life.

I told you this was a story of tragedy and ruin but there were great triumphs along the way. All except at the end, it was a fantastic ride. Today I ride a slower horse and slay the dragon of Wall Street but at a much slower pace, fitting for my 83 years of Wall Street knowledge.

Don’t confuse a bull market with genius!

In 1999 I was telling friends and relatives of an impending bear market. Literally NO ONE listened to me. It was sad as I knew they would “buy the correction” on the way down, as that simple choice of words ruled the day in the late 1990s. They were making so much money that they didn’t need me crying wolf as they had become financial geniuses. They truly believed I had lost my touch and was in fact out of touch with the reality of Wall Street and an 18-year-old bull market. I warned up until the market began its breakdown and then I said no more. It would not be a matter of I told you so and that coupled with their pain of losing money was too much for them to hear and so I went silent because I didn’t want to rub it in.

In March 2003, we were going to war with Iraq. Hussein would use his chemical weapons in defense. We would lose thousands of soldiers during these attacks. I thought to myself, THERE IS ABSOLUTELY NO REASON TO OWN STOCKS. Therefore this had to be a terrific time to buy stocks and off the market went zooming into the 2007 peak and the disaster of 2008 lying beyond. The events of 2008 were so horrific I never thought they would happen in my lifetime.

From the disaster of 2008 arose a new bull market that continues until this day . . . Thanks to the FED

(Dec 2020)

Explore posts in the same categories: UPDATE

Leave A Reply