November 2010 – T Theory® Update

T Theory Observations for November 21 2010

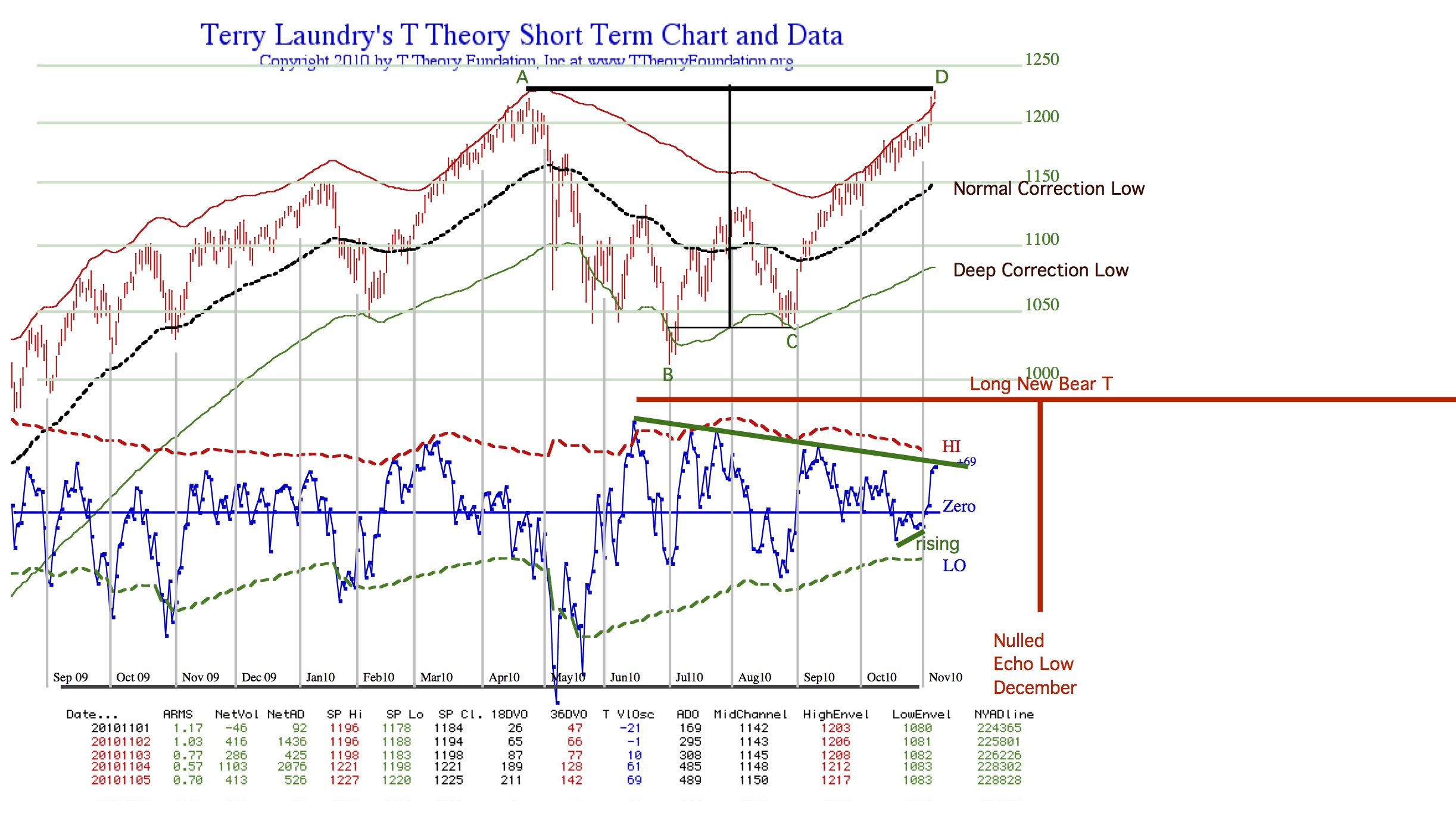

—part A———————

mp3 Commentary

Download TTOAudio20101121A

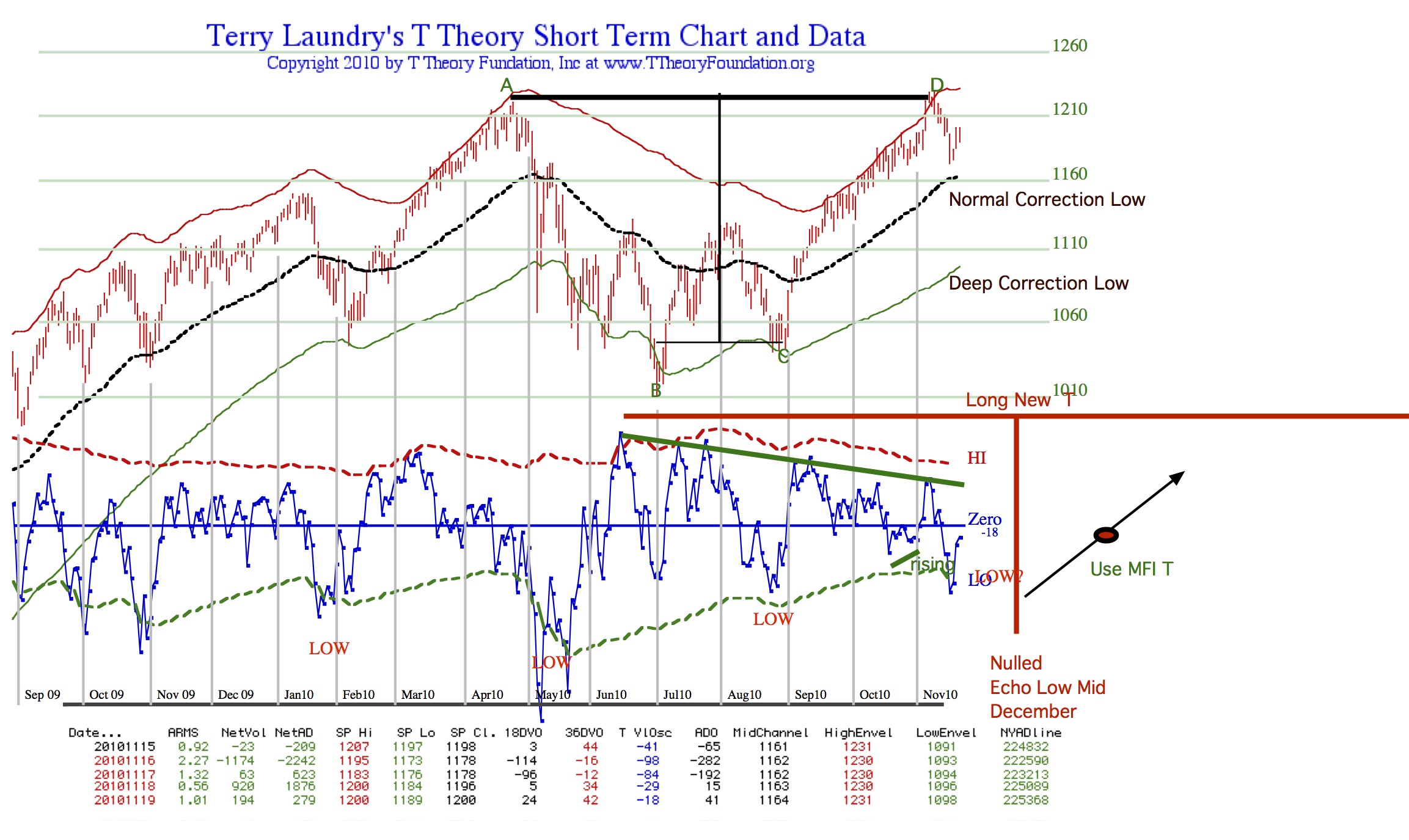

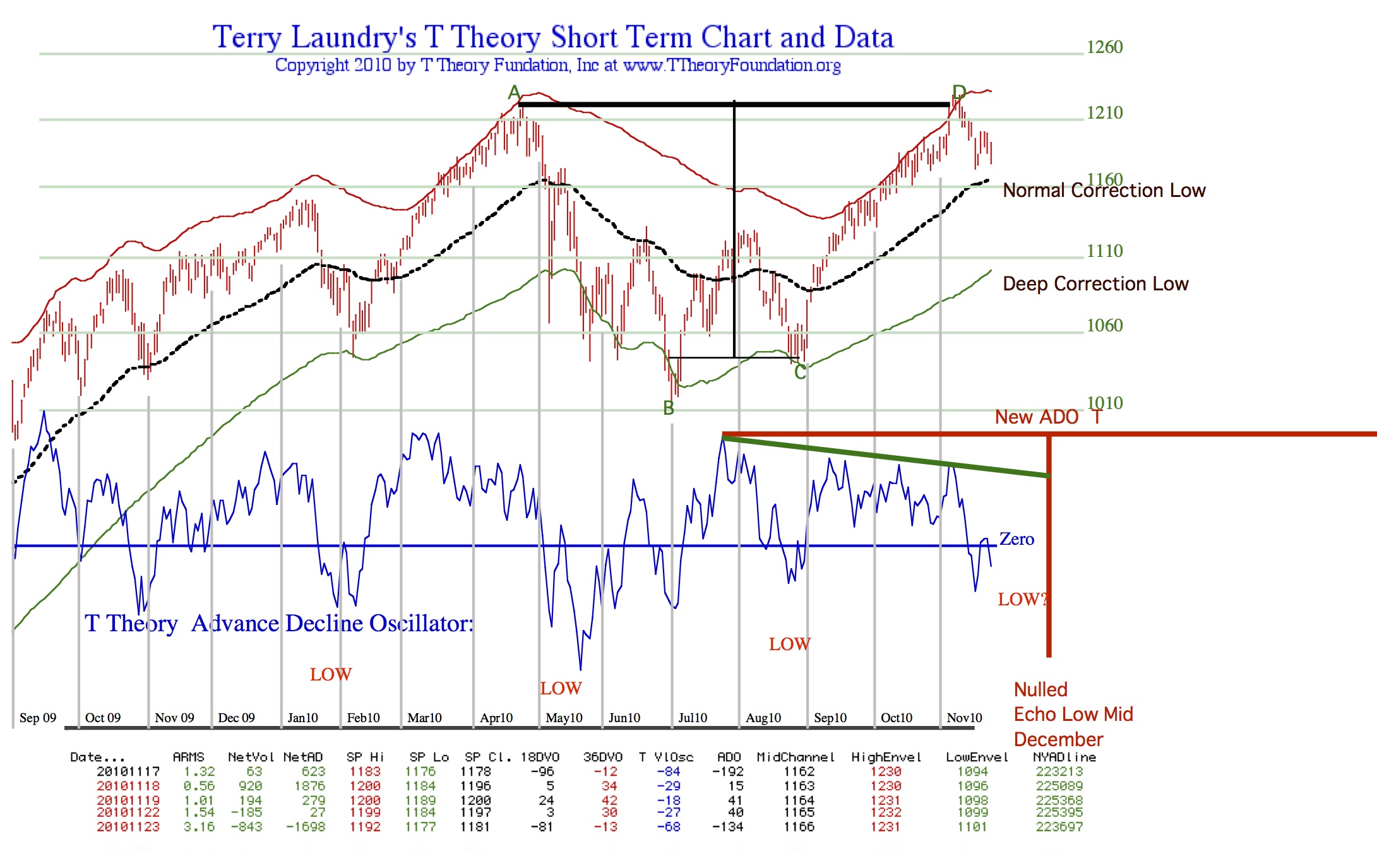

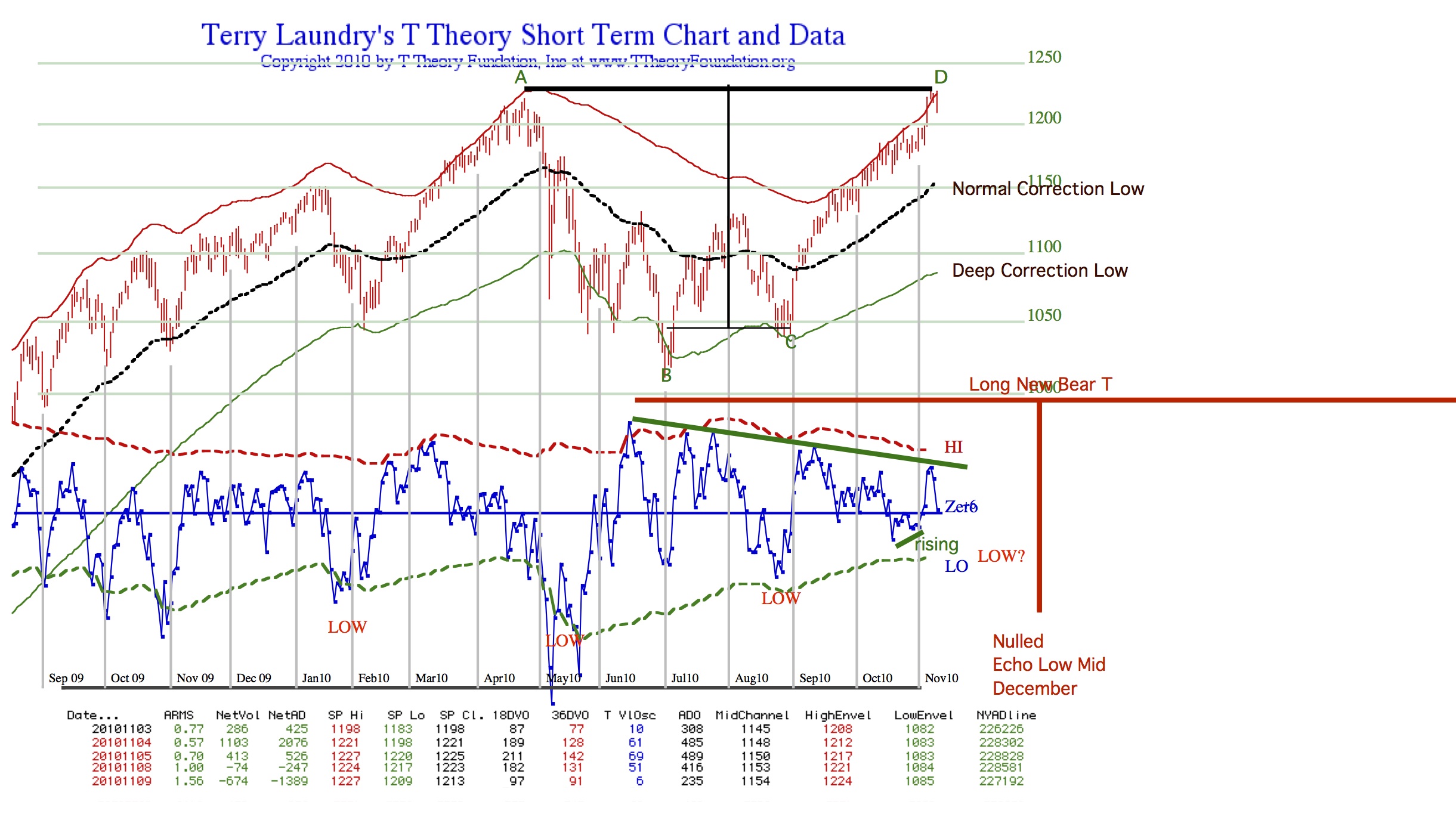

Chart

Download Next SRT20101119pdf

—part B ————

mp3 Commentary Download TTOAudio20101121B

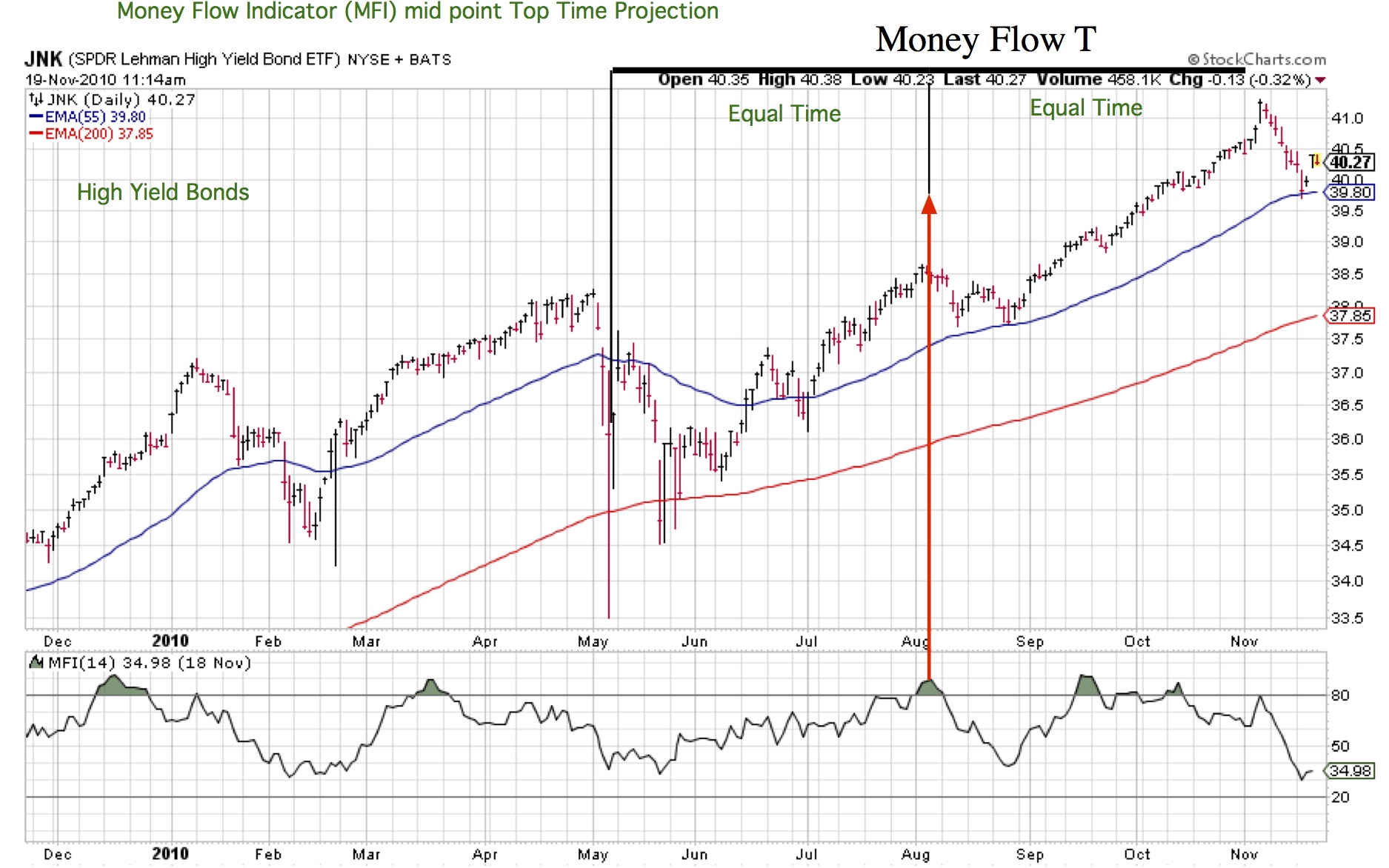

Chart

Download MFIMidPointTopProjectionforJNK20101118pdf

Download MFIMidPointTopProjectionforTLT20101112pdf

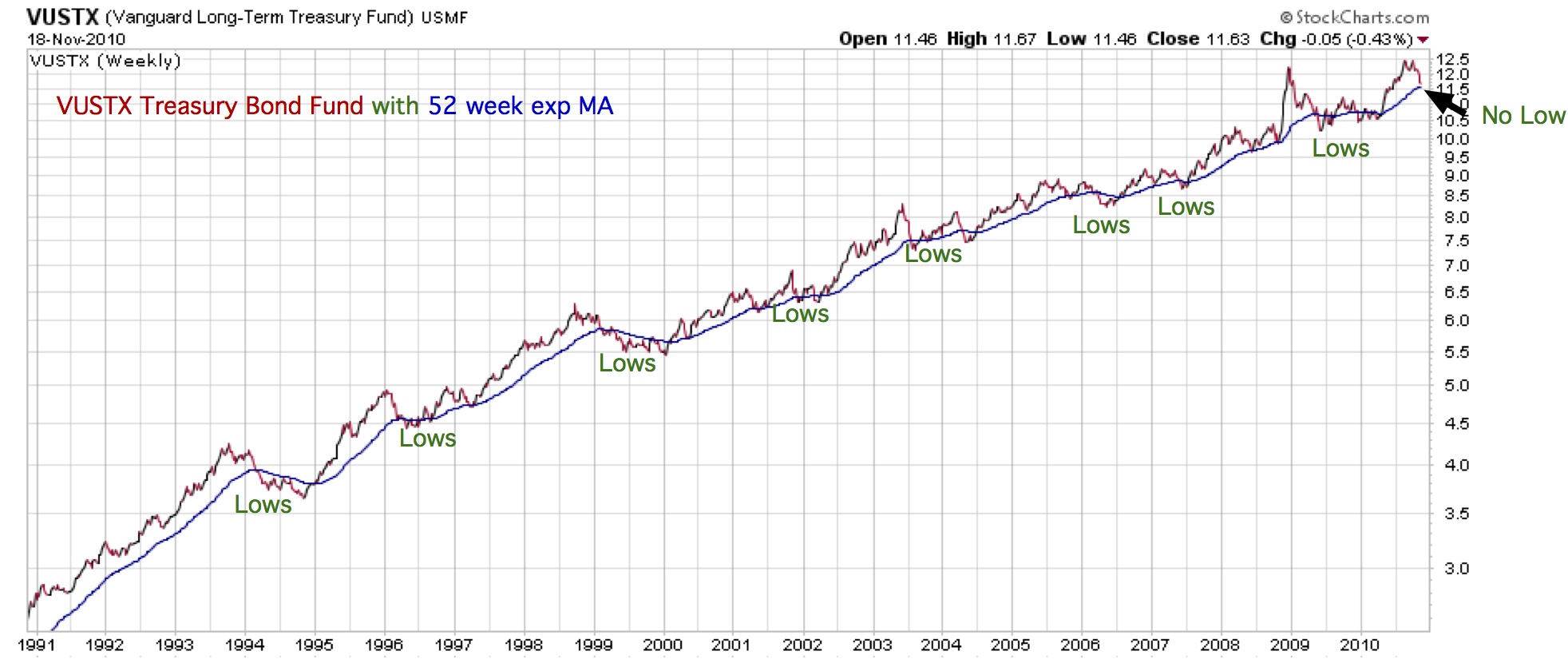

Chart

Download VUSTX with 52 week ExpMApdf

—Part C———-

mp3 Commentary

Download TTOAudio20101121C

Chart

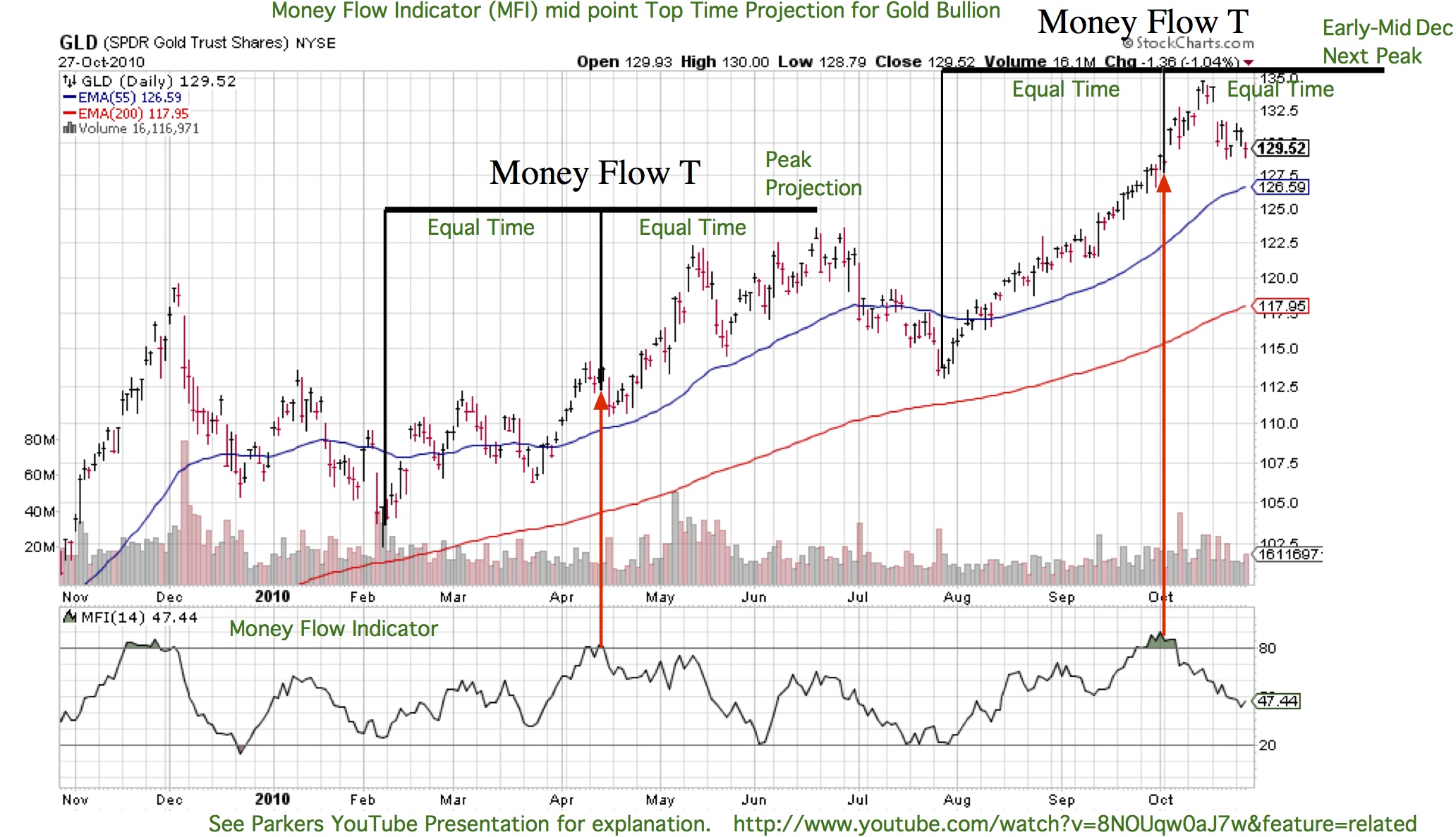

Download MFIMidPointTopProjectionforGLD20101118pdf

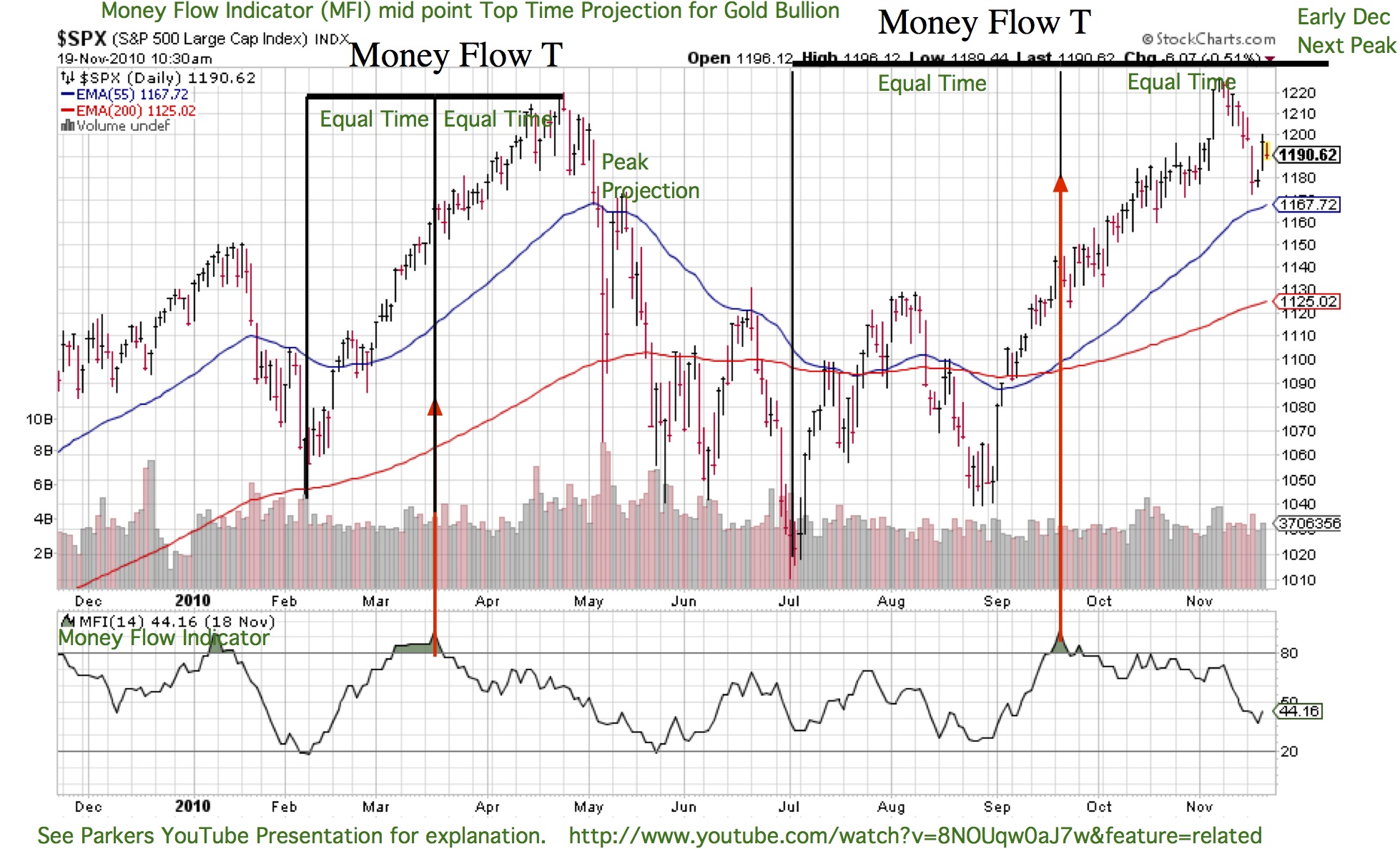

Chart

Download MFIMidPointTopProjectionforSPX20101118pdf

—Part D———-

mp3 Commentary

Download TTOAudio20101121D

PDF Chart None

—-Part E The Wednesday Mid week Update————————–

mp3 Commentary

Download TTOAudio20101124E

Chart

Download NextSRTado20101123pdf

T Theory Observations for November 14 2010

—part A———————

mp3 Commentary

Download TTOAudio20101114A

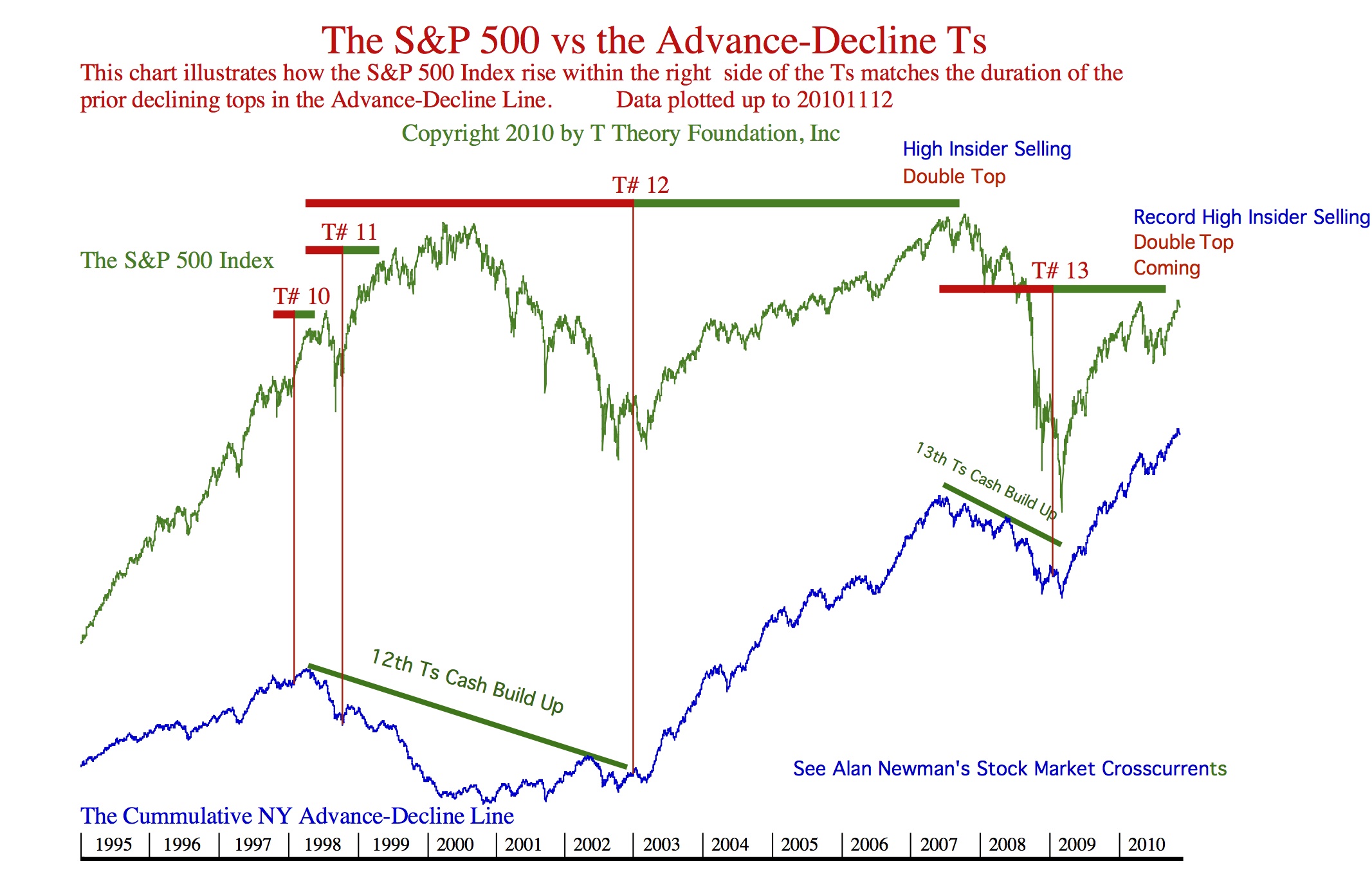

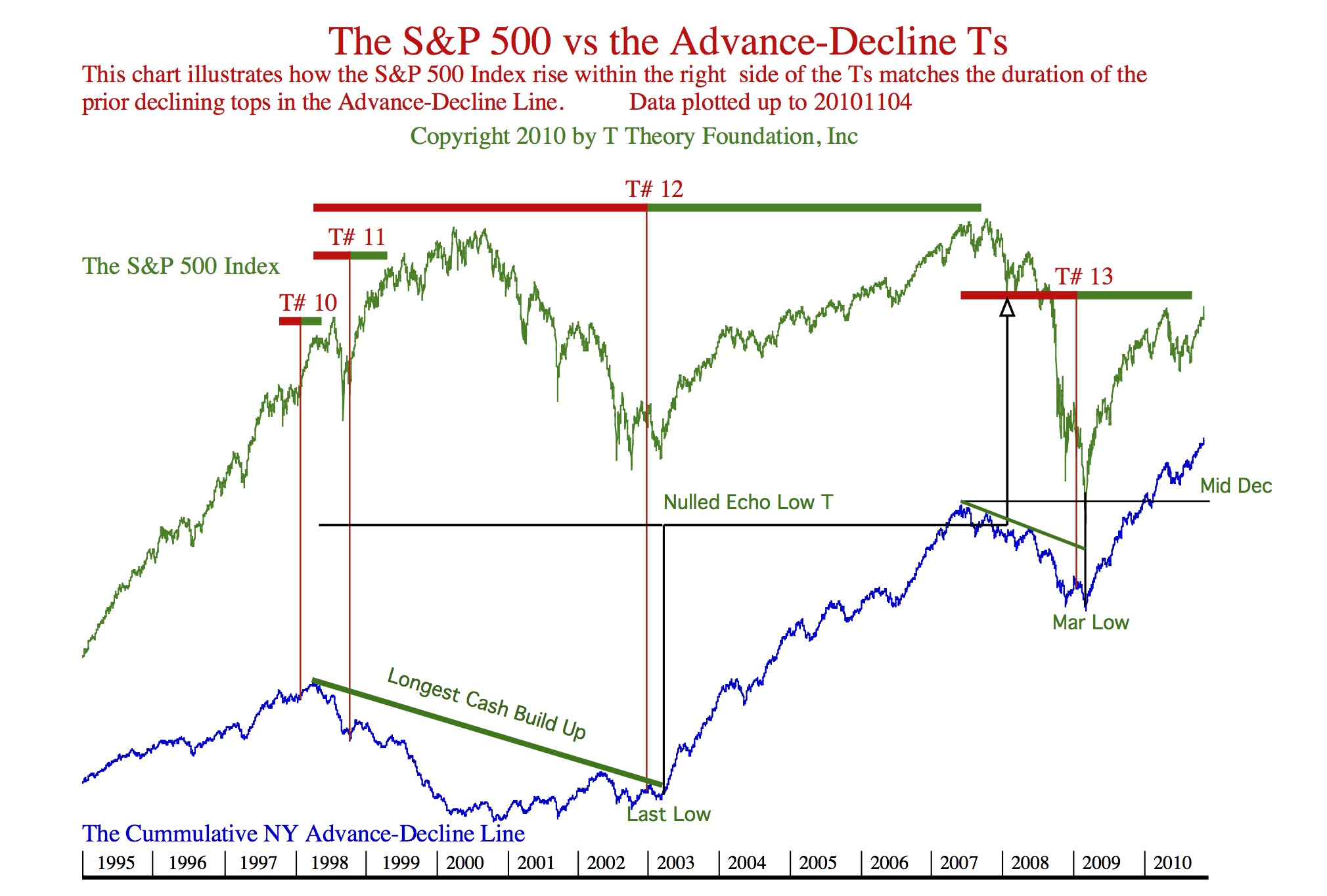

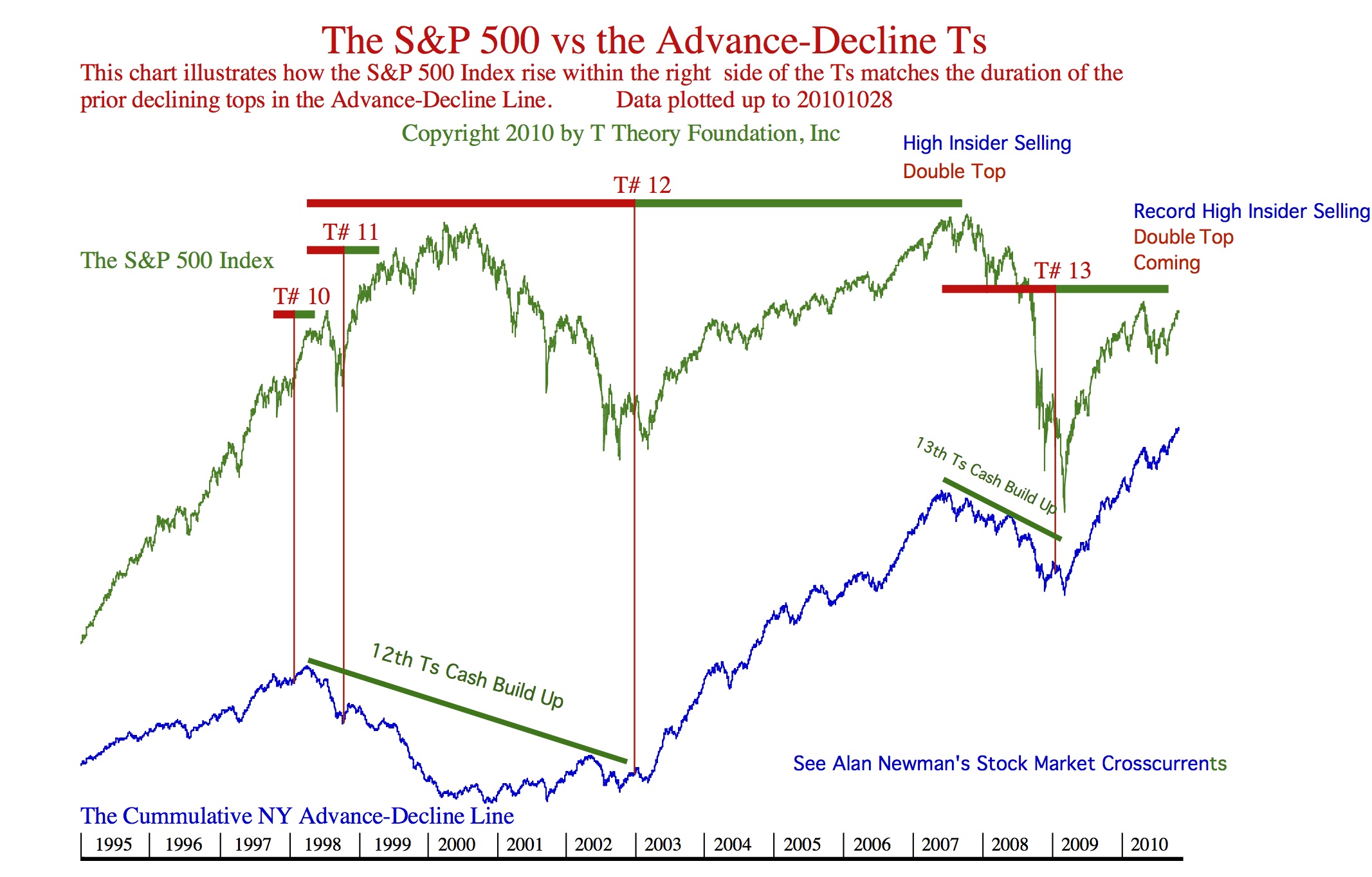

Chart Advance-DeclineTs

Download ADTs20101112pdf

—part B ————

mp3 Commentary

Download TTOAudio20101114B

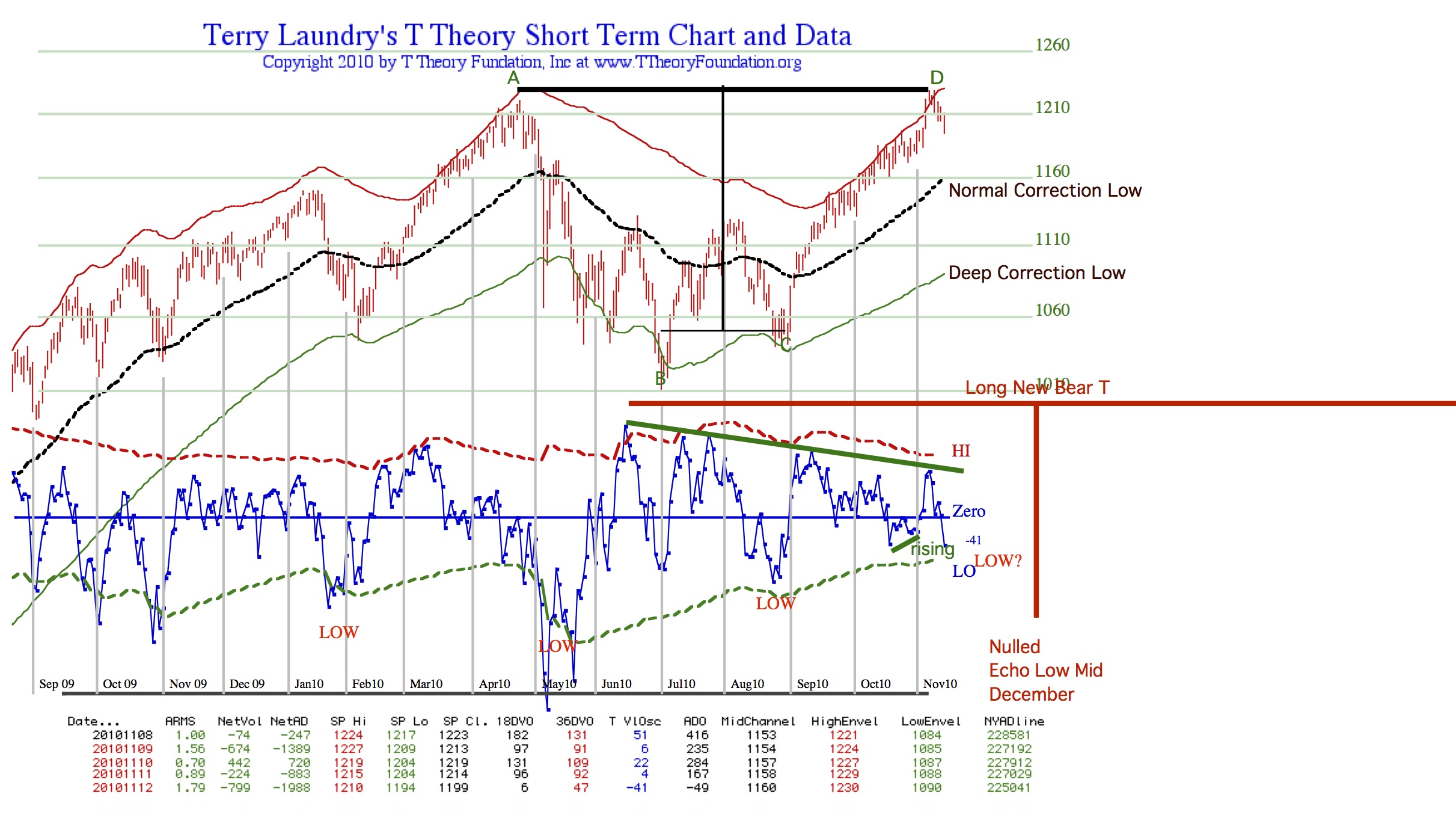

Chart

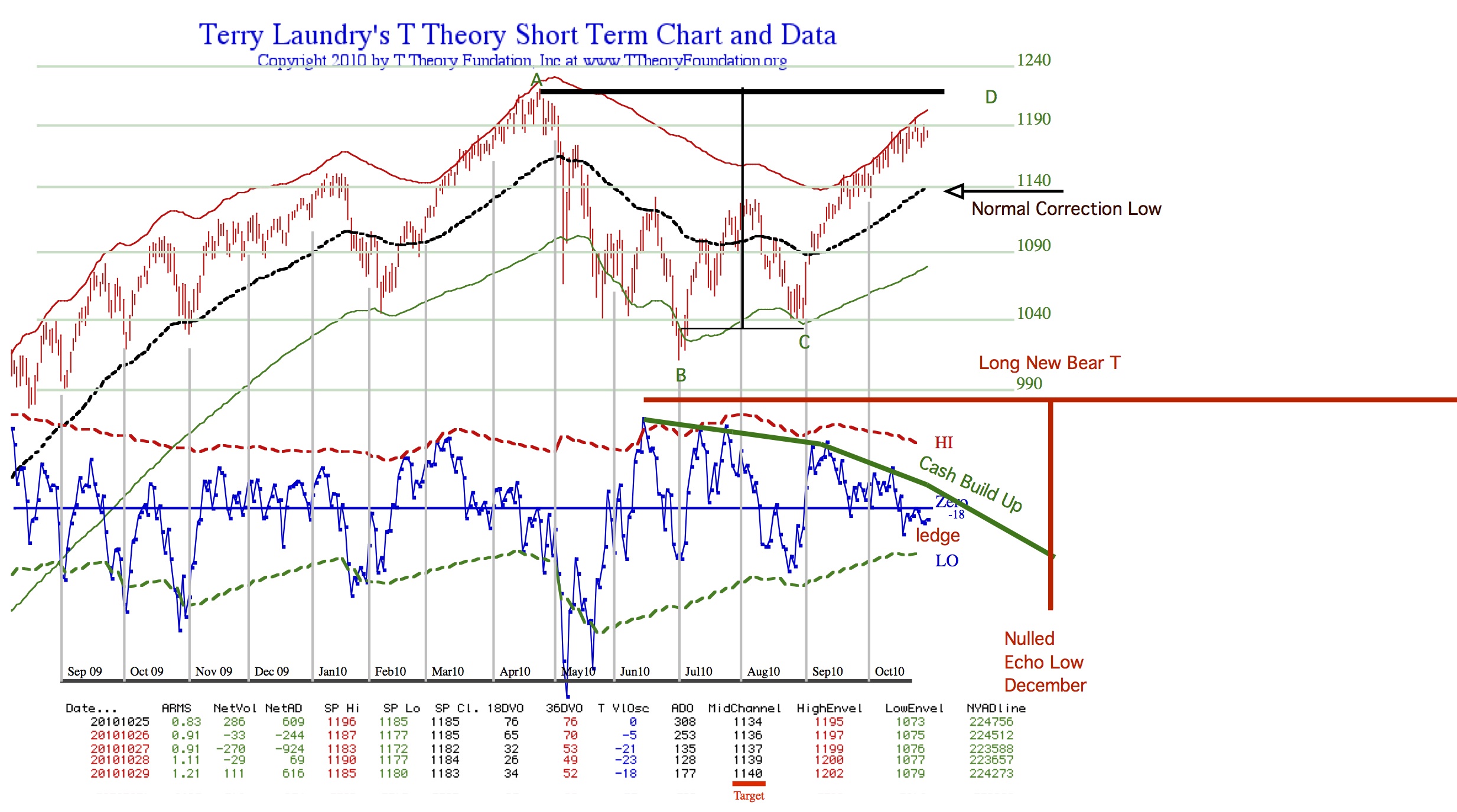

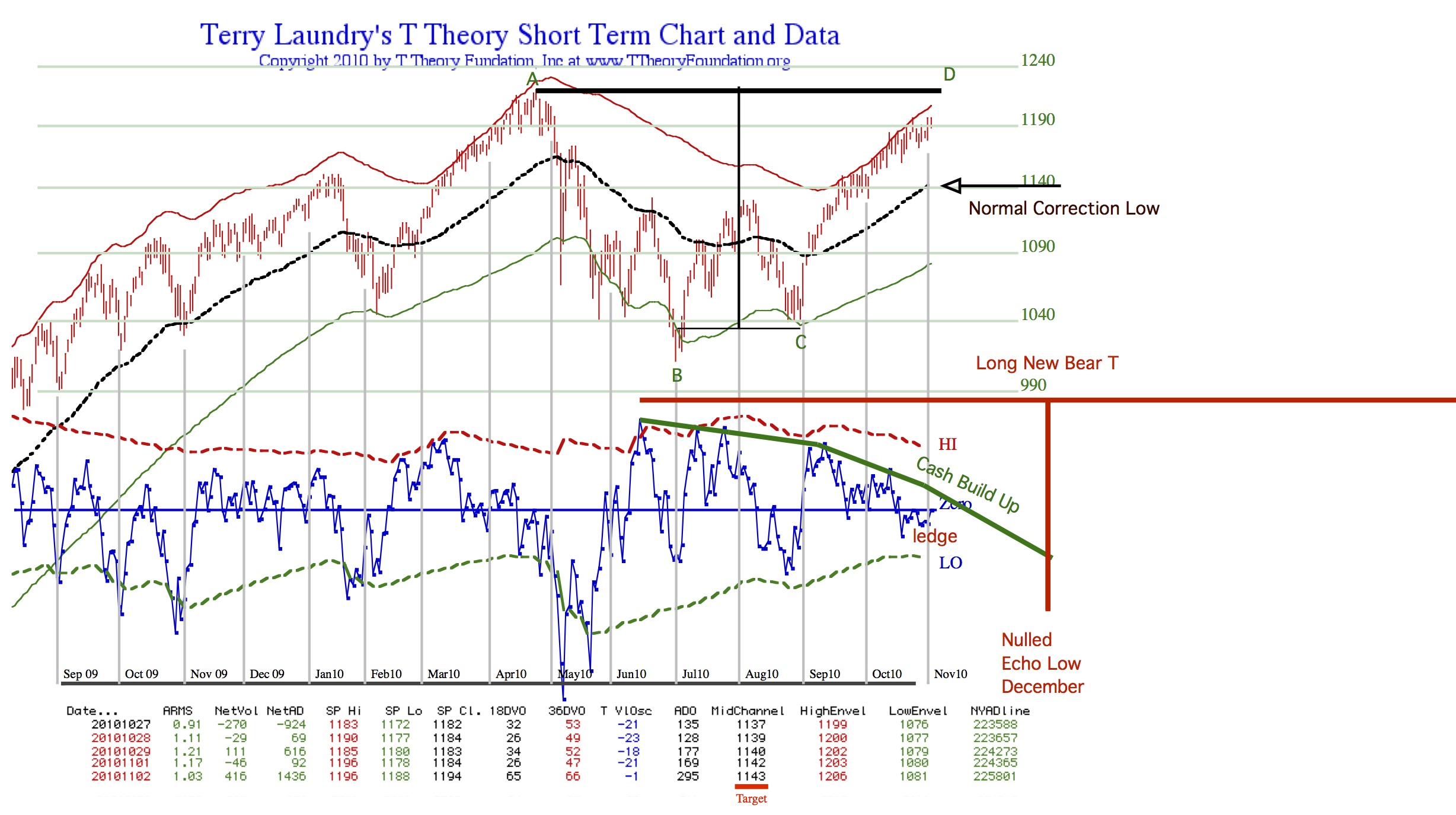

Download NextBearT20101112pdf

—Part C———-

mp3 Commentary

Download TTOAudio20101114C

Chart

Download TLT and VUSTX 3 yr Overlaypdf

Chart

Download TLT MFI 2010 peak in August

—Part D———-

mp3 Commentary

Download TTOAudio20101114D

PDF Chart

Download MFIMidPointTopProjectionforGLD20101112

—-Part E The Wednesday Mid week Update————————–

The latest Nov 17 mid week post is below.

mp3 Commentary

Download TTOAudio20101117

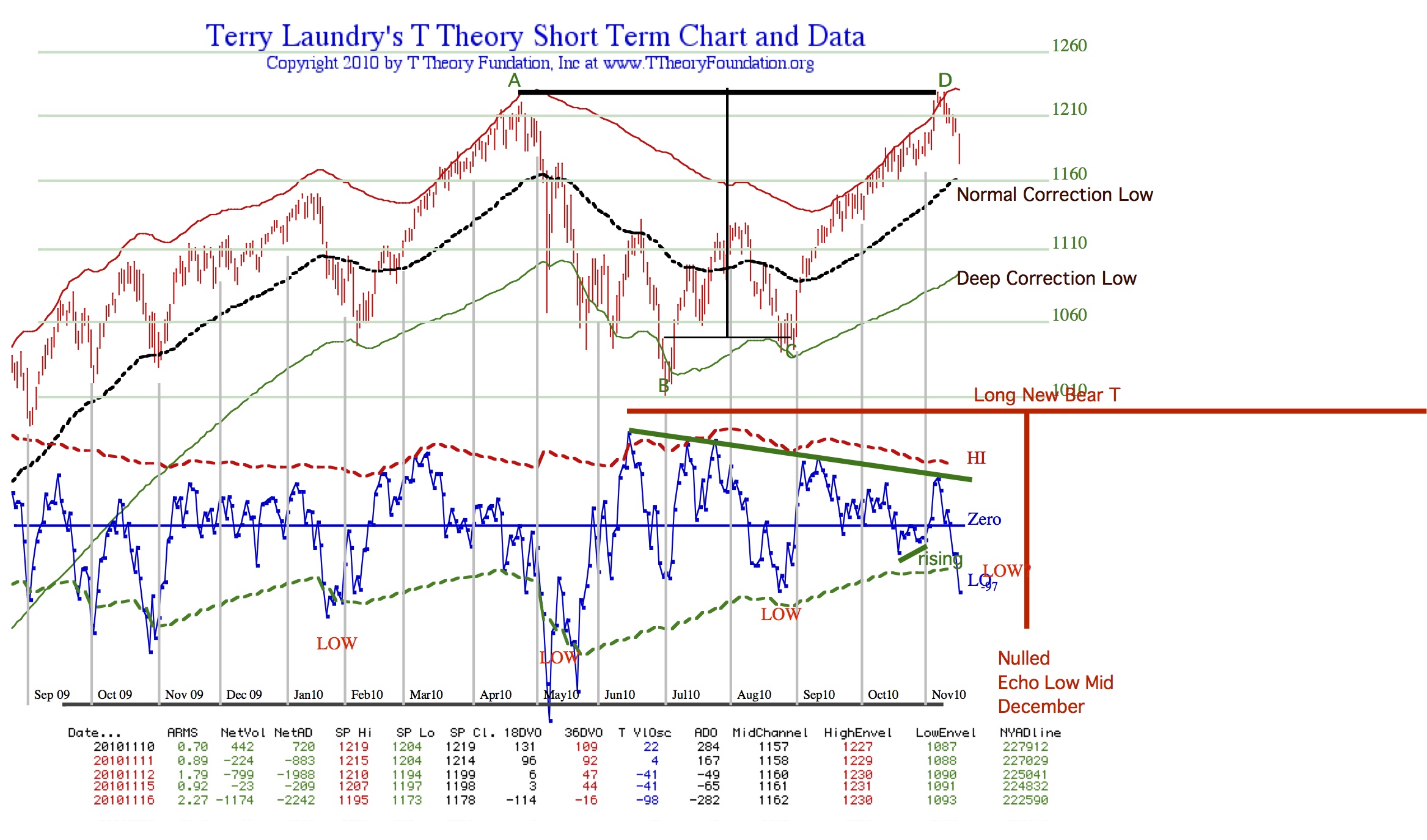

PDF Chart

Download Next Bear T20101116pdf

T Theory Observations for November 7 2010

—part A———————

mp3 Commentary

Download TTOAudio20101107A

PDF Chart

ADTs and Nulled Echo Download ADTs20101104pdf

—part B ————

mp3 Commentary

Download TTOAudio20101107B

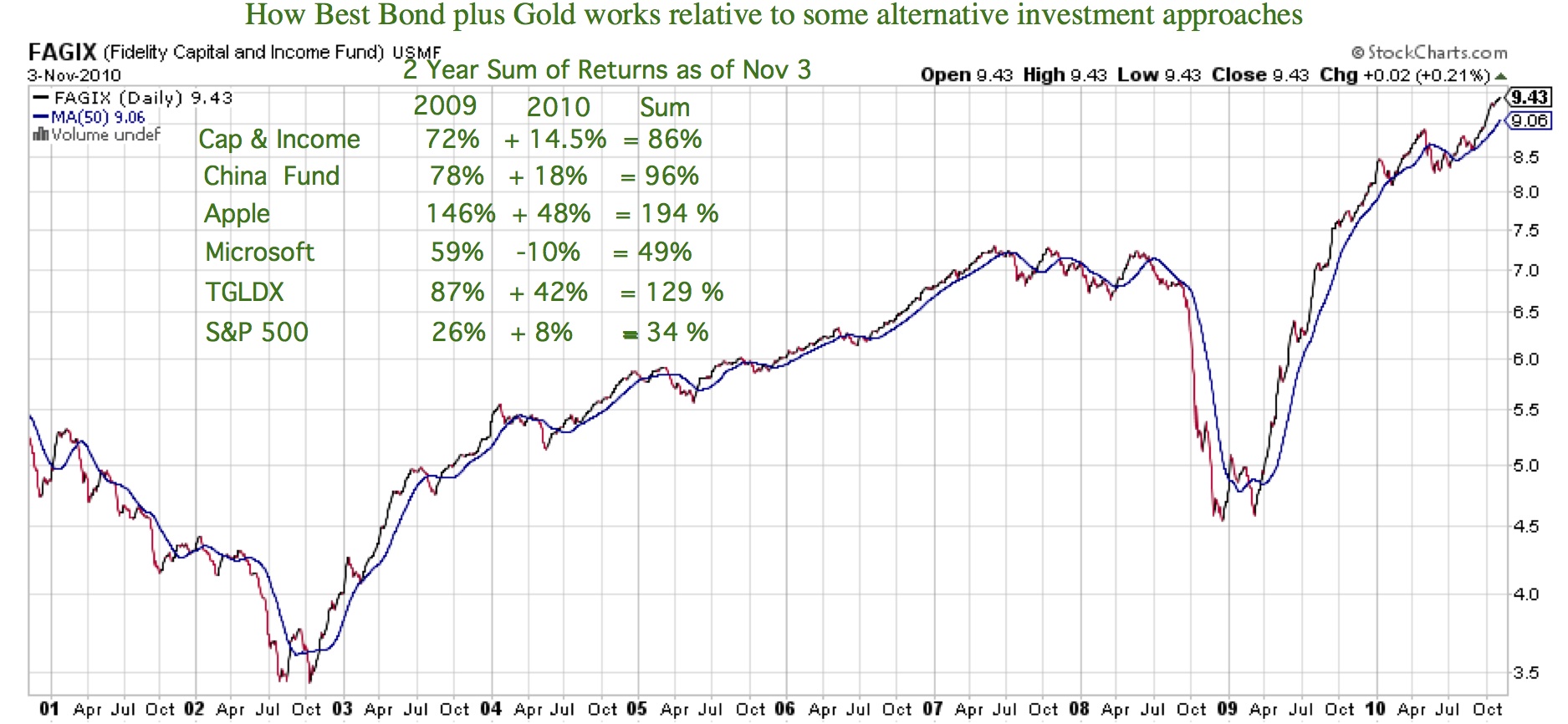

Chart Best Bond

Download BestBondvsAlternatespdf

—Part C———-

mp3 Commentary

Download TTOAudio20101107C

John Hathaway Recent Comments

John Hathaway, On Thursday October 28, 2010, 9:00 pm EDT

The world’s monetary system is in the process of melting down. We have entered the endgame for the dollar as the dominant reserve currency, but most investors and policy makers are unaware of the implications.

The only questions are how long the denouement of the dollar reserve system will last, and how much more damage will be inflicted by new rounds of quantitative easing or more radical monetary measures to prop up the system.

Whether prolonged or sudden, the transition to a stable monetary system will become possible only when the shortcomings of the status quo become unbearable. Such a transition is, by definition, nonlinear. So central-bank soothsaying based on the extrapolation of historical data and the repetition of conventional wisdom offers no guidance on what lies ahead.

It’s amazing that there is no intelligent discourse among policy leaders on the subject of monetary rot and its implications for the future economic and political landscape. Until there is fundamental monetary reform on an international scale, most economic forecasts aren’t worth the paper on which they are written.

Telltale signs of future trouble aren’t hard to spot. Only a few months ago, Federal Reserve Chairman Ben Bernanke and a chorus of other high-ranking Fed officials were talking about exit strategies from the U.S. central bank’s bloated balance sheet and the financial system’s unprecedented excess liquidity. Now, those same officials are talking about pumping more money into the system to stimulate growth.

Risky Targets

And they’re not alone: Six months ago, the chief economist of the International Monetary Fund, Olivier Blanchard, suggested that raising inflation targets to 4 percent from 2 percent wouldn’t be too risky.

This sort of talk must grate on the nerves of our trading partners, China, India, Russia and others, who have accumulated pyramids of non-yielding Treasury debt. No haven there. Return- free risk may be a better way to put it. And bickering among central bankers over currency manipulation and rising trade tensions doesn’t exactly reinforce one’s confidence in a scenario of sustained economic growth and a return to prosperity.

The prospects for an orderly unwinding of the extreme posture of global monetary policy are zero. Bernanke, Jean- Claude Trichet and Mervyn King, his counterparts in Europe and the U.K. respectively, are huddling en masse upon the most precarious perch in the history of monetary affairs. These alleged guardians of monetary stability, in their attempts to shore up the system, have simply created the incinerator for paper money. We are past the point of no return. Quantitative easing may well become a way of life.

No Freak Occurrence

The consensus investment view seems to be that the credit crisis of 2008 was a freak occurrence, unlikely to repeat. That is wishful thinking. Monetary policy has painted itself into a corner. Based on our present course, there will be more bubbles and more meltdowns.

Financial markets and institutions sense trouble, as reflected in the flight to supposedly safe assets such as Treasuries and corporate-debt instruments with paltry yields, as well as the reluctance to lend by commercial banks. We are stuck in an epic liquidity trap. The irony is, if global central banks succeed in creating inflation, the value of these safe assets will be destroyed. It is a slaughter waiting to happen.

In the pedantic mentality of central bankers, their playbook creates just the right amount of inflation. As inflation accelerates, consumers will spend to get rid of their dollars of diminishing value and spur the economy. Once consumers start spending, it will be time to raise interest rates because a solid foundation for prosperity will have been established, they say.

Slender Thread

But whatever the playbook promises, the capacity of financial markets to overshoot can’t be overestimated. The belief among policy makers and financial markets in the possibility of this sort of fine-tuning is preposterous, but it is the slender thread on which remaining investment and business confidence rests.

The breakdown of the monetary system will be chaotic. When inflation commences, it will be highly disruptive. The damage to fixed-income assets will seem instantaneous. Foreign-exchange markets will become dysfunctional. The economy will become even more fragile and unpredictable.

Gold is an imperfect, but comparatively reliable, market gauge for the extent of current and future monetary destruction. The recent acceleration in the dollar price of the metal to $1,381, a record high in nominal terms, coincided with talk of a new round of quantitative easing and highly visible discord among major nations on trade and currency-valuation issues.

Naysayers’ Bubble

Naysayers point to gold’s price and see a bubble, without understanding that the only acceleration that is taking place is in the rate of decline of paper currency. The Fed is organizing an attack on the dollar’s value, believing that this is the most expedient way to defuse deflationary market forces. The man in the street is unaware, a perfect setup. Inflation can only be successful when the public doesn’t see it coming.

The sudden torrent of commentary on gold isn’t the sign of a bubble. Anti-gold pundits provide a great service to those who grasp this historical moment: They facilitate the advantageous positioning of the one asset most likely to be left standing when the dust settles.

(John Hathaway is a managing director of Tocqueville Asset Management LP in New York. The opinions expressed are his own.)

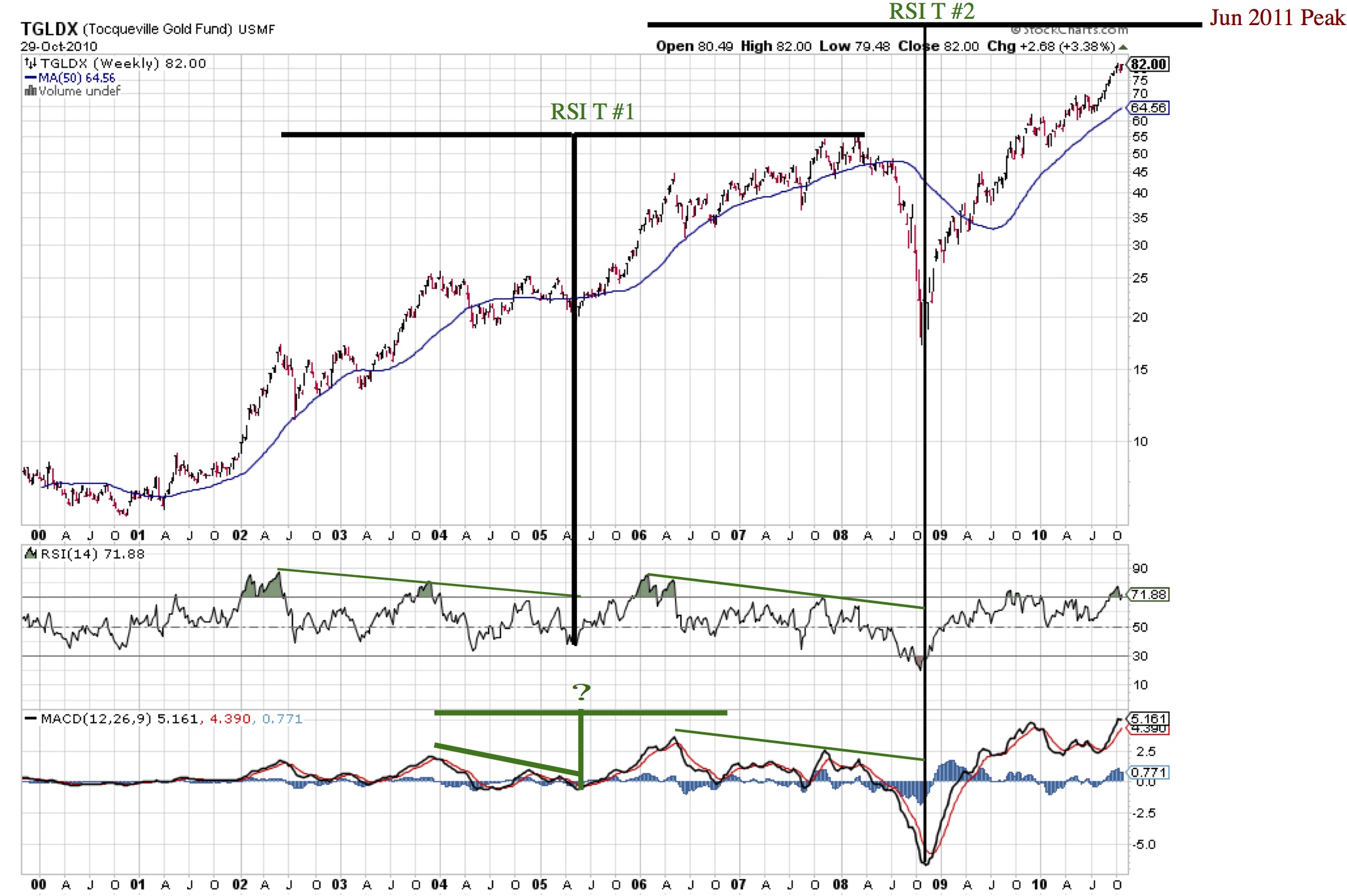

PDF Chart

Tocqueville Gold Fund

Download TGLDX LT GoldTspdf

—Part D———-

mp3 Commentary

Download TTOAudio20101107D

PDF Chart Next T

Download Next Bear T20101105pdf

—-Part E————————–

The Nov 10 mid week post is below.

mp3 Download

TTOmidwkAudio20101110

PDF Chart

Download Next Bear T20101109pdf

T Theory Observations for October 31 2010

—part A———————

MP3 Audio

Download TTOAudio20101031A

Chart#1

Download ADTs20101028pdf

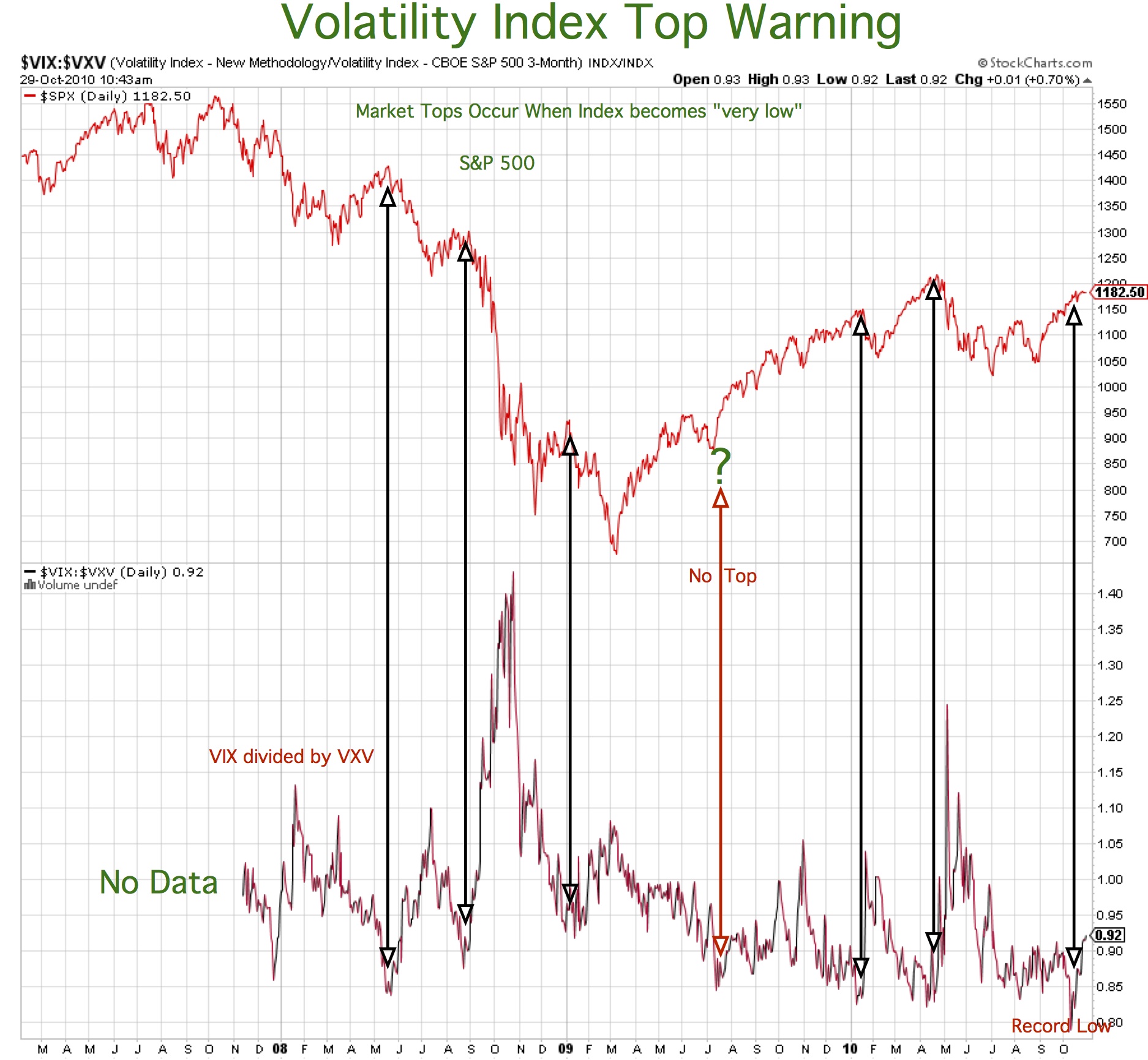

Chart#2

Download Volatility Index Top Warning20101028pdf

—part B ————

MP3 Audio Download TTOAudio20101031B

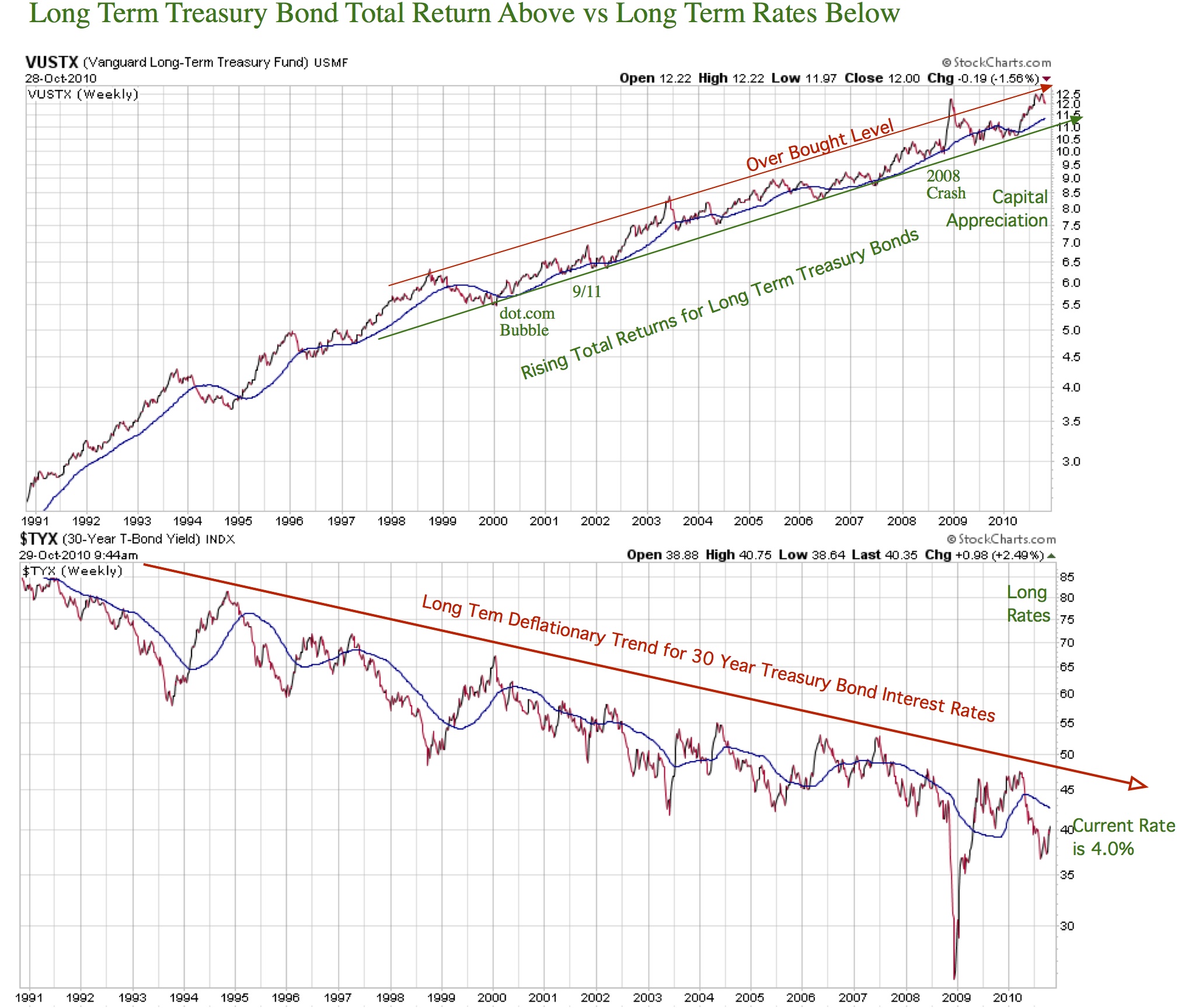

Chart#1

Download LTTreasury Return vs Long Rates20101028pdf

Chart#2 None

—Part C———-

MP3 Audio

Download TTOAudio20101031C

Chart#1

Download MFIMidPointforGLD20101027pdf

Chart#2 Note from Mike

I enjoyed this Sunday’s (early) update as usual. However, in it you asserted that it was necessary to have a $190/yr subscription in order to view ratio charts such as $VIX:$VXV in StockCharts. That is patently incorrect.

I have never had a subscription and I have no difficulty creating ratio charts that go back 3 years (there is that limitation on how far you can go back if you don’t have a subscription). For example, on my computer http://stockcharts.com/h-sc/ui?s=$NYAD:$CPC&p=D&yr=3&mn=0&dy=0&id=p76301796904 displays back to November 2007.

Furthermore, on the StockCharts “Perf” charts, the backdate limit is longer. For example, the chart http://stockcharts.com/charts/performance/perf.html?tlt,GLD goes back to late 2002. (But on perf charts you can’t create ratios. You can create differences rather than ratios, by clicking on the rectangular tabs, but I don’t think that you’d want those.)

—Part D———-

MP3 Audio

Download TTOAudio20101031D

Chart#1

Download Next Bear T20101029pdf

Chart#2 None

—-Part E————————–

Nov 3 Post

MP3 Download

TTOAudio20101102E

Download

Next Bear T20101102

****************************************************************************************

All Rights Reserved By The T Theory® Foundation ©

Order the T Theory® Encyclopedia

For a complete understanding of the T Theory® and how to successfully use Terry’s unique methods, order the Encyclopedia from Paula at the above link. There is additional material in the encyclopedia not covered here. Paula will be more than happy to answer your questions too.

Many thanks to Paula Burke for her permission to re-post Terry’s old T Theory® explanations. The period re-blogged on these pages are some of Terry Laundry’s best work and was published here from public domain.

****************************************************************************************

I claim no credit for the material found under T Theory® on this blog. All of this material is the creation of Terry Laundry and was downloaded from Terry’s free blog site (TypePad). I have created a mirror of Terry’s original material and now there is a second site containing Terry’s T Theory®. One or both of these websites hopefully will survive through time as Terry’s material is too important to be lost to the ravages of time. This site is simply a memorial to his lifetime work.

The page content re-blogged here is exactly as Terry created on his original webpages (saved on my computer with ScrapBook)). Nothing has been left out from the period Dec 2003 to June 2011. From Terry’s site, I made a lot of formatting changes, creating a more easily readable webpage appearance. The PDF chart duplicates of the JPEGs have been omitted for ease and speed of recreating Terry’s pages. References to PDF charts should be ignored (but no chart was left out).

After June 2011, Terry created a paid subscription website. None of that material is found here.

There were many many, many hours spent on this project; downloading Terry’s individual charts & audio files, followed by the uploading of Terry’s charts and audio to my WordPress blog library, after which I had to insert the uploaded material into my new T Theory® webpages (hopefully in the correct places). This was a dull and arduous project and I hope you enjoy it. I don’t believe there remains any more of Terry’s material in free domain, so my T Theory® project is probably finished. If I’ve missed something, you can leave me a comment.

If you find an uploaded reference error (chart or audio in the wrong place), please note the month and year of the webpage, plus the exact name of the referenced error file. Include any other info that will help me locate the problem file and where it occurs on the webpage. Leave a comment for me with the info and I’ll fix it.

Terry’s material is very long and will take many weeks for you to finish. Don’t hurry, it’s not a marathon and you will absorb more if you go through it at a reasonable rate. This is especially true for those who don’t invest in the T Theory® reference encyclopedia. The encyclopedia is a written reference for T Theory® and includes everything of importance for Terry’s T Theory®. Without the reference encyclopedia you must depend on your memory and Terry’s method carries some rules that you could easily violate. The encyclopedia also includes new information never seen on his website.

You are welcome to save any or all of my blog material to your computer. You also have my permission to re-blog my information, but you must (1) credit me and my blog in an obvious manner and (2) don’t change my material.

FYI – I find the best way to save a webpage is using “ScrapBook” (it’s an add-on for the FireFox browser). ScrapBook saves a webpage to your computer EXACTLY as it appears on the day you saved it. You can’t tell the difference between the internet webpage and your ScrapBook saved webpage. The saved pages are not pictures. Instead the pages consist of HTML and page functionality remains identical on your computer. There is also a second method for using ScrapBook, where you can save all of the webpages down to a defined link depth. This optional method means all links will function on your computer to the link depth specified (meaning you can click on links on your saved webpages and tunnel down into pages within pages). Saving the normal way will only save the top webpage but the links that exist could continue to function by taking you to the website on the internet instead of on your computer. But sometimes the linked website doesn’t exist anymore. I’ve had this happen on some very good webpages with unique information (they just disappear into the internet void). That’s a bummer when you lost some really good info and thus rose my need for ScrapBook. You can also filter the pages saved using the optional ScrapBook method, which can exclude all pages not coming directly from the specified website (filtering is recommended using this method otherwise you wind up with a LOT of useless stuff).

.

Explore posts in the same categories: . . . T Theory®

Leave A Reply